Financial advisors need to affiliate with a broker-dealer (BD) or registered investment advisor (RIA) in order to sell investments (other than annuities) within DC plans.

There are three basic platforms they can choose from:

1. Wire houses, or those platforms where the plan advisor is an employee

2. Independent BDs, where the advisor is a 1099 contractor

3. RIAs, where the advisor has no affiliation with a BD

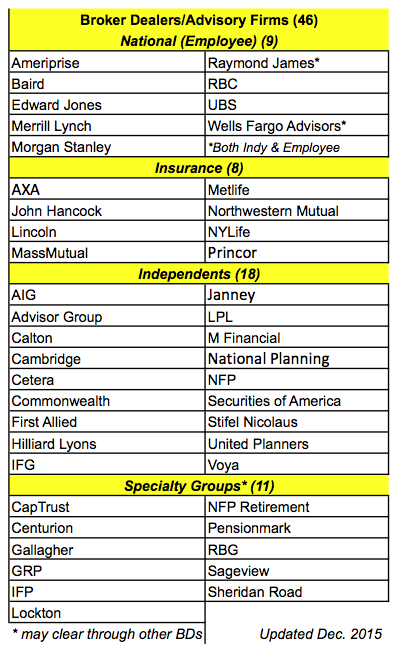

But like most things in the defined contribution business, it’s not that simple. Most experienced plan advisors these days fall into a category called “hybrids,” meaning they affiliate with a BD and an RIA. That RIA can be owned and controlled by the BD with which they are affiliated, or the advisor can own and run it independently. Furthermore, there’s a growing crop of specialty groups, many of which are affiliated with an established BD, that focus on supporting plan advisors. Some of those groups require a BD or RIA change, while others do not.

Some experienced advisors are joining these specialty groups to leverage their intellectual capital and support as well as the brand. As with BDs, some require the advisor to be an employee, while others allow advisors to remain independent. Other advisors choose to remain independent, usually affiliating with a BD that has allocated at least a minimal amount of support in the form of home office personnel and the tools that advisors need to run a DC practice.

But with 250,000 of the 300,000 active advisors being paid from working with a DC plan, a majority of these advisors are affiliated with BDs or RIAs that do not have much, if any, support or personnel dedicated to DC plans. Experts predicted a mass exodus from these distributors when the ERISA 408(b)(2) rules were promulgated in 2012 because advisors had to declare whether they would be acting as a fiduciary along with the fees they would be paid.

Though 408(b)(2) did have some impact on advisor movement, like Y2K it was not as much as some experts had predicted. The DOL’s pending conflict-of-interest rule may change that, for two reasons: (1) most advisors that even touch a plan will be considered ERISA fiduciaries; and (2) the rule may affect how both advisors and BDs deal with IRA rollovers.

Stay tuned for changes that, though affected by the DOL rule, will be driven mostly by market dynamics as plan advisors look for platforms that support their practices and more specialty groups emerge — dynamics evidenced by the robust list of distributors below. (To view the list in pdf format, click here.)