To view a PDF version of this article, click here.

At a retirement conference two years ago, the big buzz was about Big Data, and how it would revolutionize retirement plan management.

The promise was that by having the ability to look at employee behavior in a very granular way, we could identify areas of need and target efforts accordingly.

Sometimes that works and sometimes it doesn’t. People like magic bullets, but magic bullets don’t always shoot straight. Data is nothing more than a collection of numbers, which can be interpreted in many ways.

Knowledgeable interpretation can reveal valuable clues on where to direct efforts. Less knowledgeable interpretation can lead to misleading conclusions, and potentially move a plan further from its goals. A seasoned retirement plan advisor can be a knowledgeable interpreter.

Some of the challenges with “readiness metrics” include:

- There are no industry-standard readiness reports. They vary widely among providers, in both content and

- Unscrubbed or incomplete data, from the employer or recordkeeper, can turn otherwise useful reports into

- Readiness forecasts can be wildly inaccurate unless individuals volunteer information about other retirement assets they may hold (outside the workplace plan) or other retirement income streams they may be

- Reports provide “dots,” but humans connect them, with greater or lesser

Who Cares About Readiness, Anyway?

Good advisors care. They understand how to utilize success metrics to generate better employee outcomes, thereby demonstrating value. On the employer side, we have encountered a wide range of awareness and interest regarding readiness metrics and their potential value. Some employers might mistake the ADP test results as the only important “success metric” — pass the test, no one yells; fail the test, big shots yell. Part of our job, as an industry, is to make employers more success-centric. Many of them have never thought about how to define and measure “success” within the context of their retirement plan.

Often, employers offer a retirement plan because it’s an expected part of the benefits package, and they haven’t really thought much about its higher purpose. If prompted, most of them would have trouble disagreeing that the higher purpose of their retirement plan is to help employees achieve a dignified retirement. A successful plan is one that is effective to that end.

Beyond doing the right thing, there is emerging research to support the idea that getting employees on a path to retirement security actually makes good business sense. It can increase productivity, reduce turnover and allow older workers the option to exit the workplace earlier. Whatever their motivation, most employers would support the idea that it’s better to have employees who aren’t preoccupied with worry over their future.

Once Defined, It Can Be Measured

Simple, traditional success metrics, such as participation rate, deferral rate and investment diversification are widely available today, and serve as useful measurements of the current state of a plan. Competitive forces are pushing providers to offer increasingly sophisticated reporting, such as: breaking out the basic metrics by age, income level, and location; and diving deeper into the asset allocation piece (holding one fund is no longer automatically bad, if it’s an asset allocation fund). This additional granularity can help the advisor to shape education campaigns and to focus platform resources such as targeted mailings.

The newest generation of readiness reports project future income replacement ratios. They take each participant’s current balance, age, savings rate, assumed rate of return, and retirement age and project forward. Some add the ability for participants to include other retirement assets and retirement income streams and to fine-tune other inputs.

The system then projects the retirement income stream that would result, adds in the expected Social Security benefit and expresses the result as a percentage of pre-retirement income that would be replaced in retirement. Non-participating employees are factored into these reports using only their projected Social Security payments. The output shows what percentage of income the workforce is on track to replace in retirement. This can then be compared with a plan-level goal, such as 75%.

The income replacement analysis is much more sophisticated than the basic success metrics outlined earlier. But, does that mean it’s necessarily better?

Let’s argue this both ways:

- Argument #1 — Forget the fancy colored reports. The goal is to enroll every possible employee, to get them to save as much as they can afford to, to get them into a risk-appropriate investment mix, and to help them to stick with this plan through thick and thin. I don’t need any fancy metrics to accomplish this. Everyone deferring zero is a candidate for enrollment and can be easily targeted as such. If the plan offers a match, everyone saving below the match threshold can be targeted for a special reminder about the “free money” they are Everyone else can be encouraged to escalate their savings rate annually or concurrent with a pay raise that may be forthcoming. It’s better to get people to do what they can than to set unrealistic savings goals that may demoralize them right out of the plan. The investment education piece (get the right mix and stick with it) needs to be done in any event. Basic traditional metrics are enough for the advisor and the employer to keep the plan moving in the right direction.

- Argument #2 — Bring on the fancy colored reports. If the goal is to replace income, let’s focus on that. Without the knowledge of how much income the participants are on target to replace, we’re flailing away in the dark. If they need to raise their saving rate, delay their retirement date or boost their rate of return, let’s let them know that.

Which Argument Is Right?

It’s hard to argue against the basic blocking and tackling advocated in the first argument. Why wouldn’t you want to recruit every possible employee to participate? Why wouldn’t you turn them upside down and shake all the possible coins from their pockets into a plan account And, why wouldn’t you want them in investment allocations that are risk-appropriate? All that makes sense.

On the other hand, why wouldn’t you want specific data on how many of the employees are on target to replace a reasonable percentage of their pre-retirement income? If that’s the goal, let’s face the reality of where the plan stands. If readiness reports provide the level of granularity to identify individuals that are in need of work, that’s really helpful.

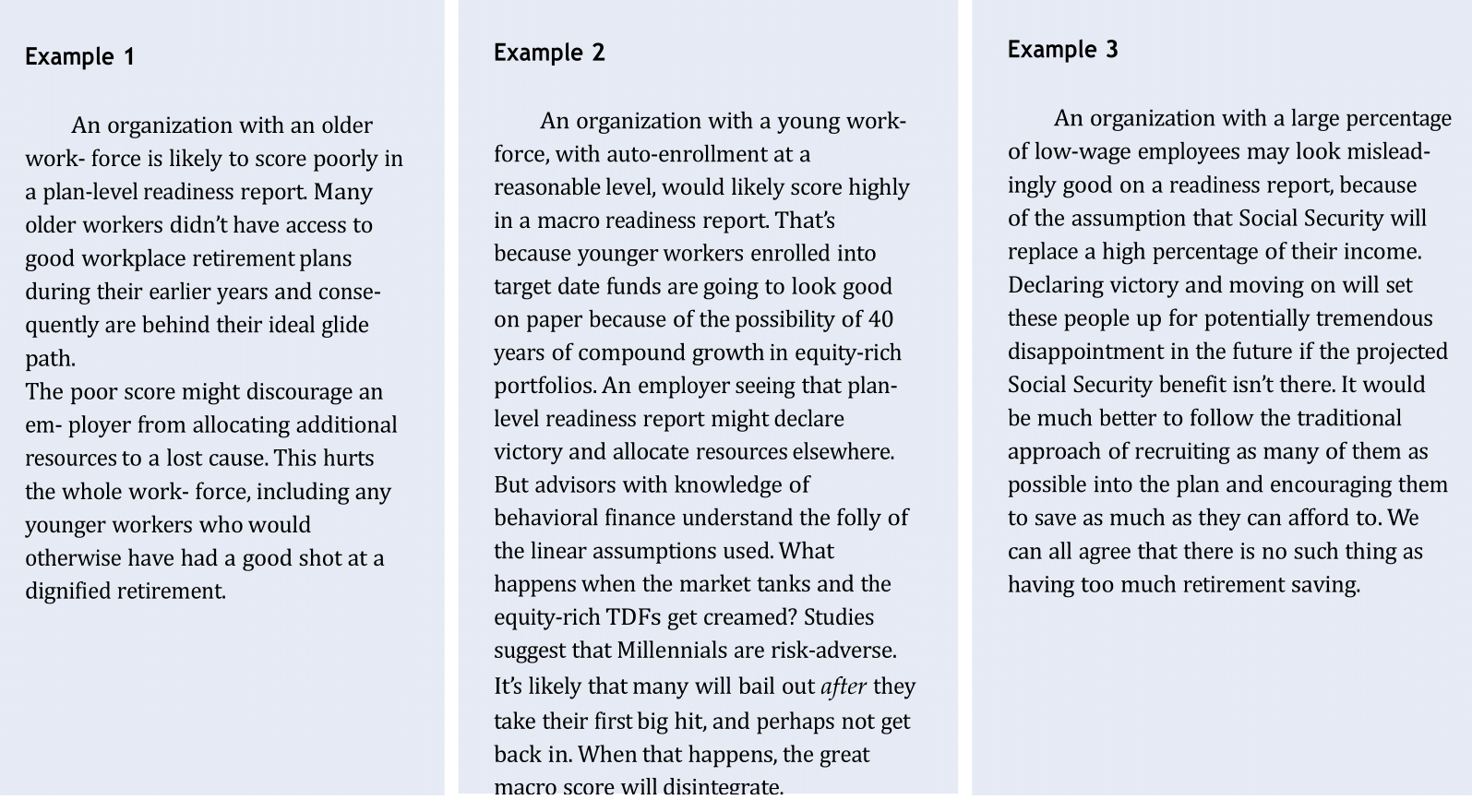

However, some readiness reports are plan-level only. There are real problems potentially with judging a plan’s success and allocating valuable resources based on macro readiness data. Figure 1 offers three examples to make this point.

Summing it up

Reports are tools. Tools can do serious work or serious damage, depending upon whose hands they are in. Seasoned advisors know how to use these tools to create better outcomes. Different plans come with different tools, so it is the advisor’s job to analyze each situation using the most appropriate approach, applying common sense, behavioral finance lessons, capital market expectations, and knowledge of the unique character of each workplace.

Relying solely on the output of macro-level readiness reports can lead to a misdirection of important resources. We should push platforms to get as granular as possible in the metrics they provide. Action, based upon thoughtful analysis of detailed data, will lead to the best outcomes.

Jim Phillips is the President of retirement resources. He has been in the investment industry for over 35 years, and has been focused in the area of qualified retirement plans since 1995.

Vice President Patrick McGinn is a CFA charterholder and has been in the securities industry since 1993. He holds the chartered Financial Analyst® designation, is an Accredited Investment Fiduciary, and is a member of the Boston Security Analyst Society.

The advisory team at Retirement Resources in Peabody, Mass., represented by Jim Phillips and Patrick McGinn, AIF, cFA, is the 2015 NAPA 401(k) Advisor Leadership Award winner.

This article originally appeared in the June 2015 Special Outcomes Issue of NAPA Net the Magazine.