By Paul R. Samuelson, PhD and Warren Cormier

Ask any plan sponsor and they will tell you that maximizing (or at least enhancing) their participants’ retirement readiness is a key goal of offering a DC plan (along with being competitive in labor markets). Ask them how they plan to achieve this, plan sponsors will respond by saying they basically offer the DC plan and in most cases offer matching contributions and some form of education and guidance. They will also tell you they look to advisors, record keepers and DCIOs to help them achieve that goal.

Approaches to retirement readiness in the DC industry have largely been focused on the accumulation phase: deferring income, proper asset allocation, avoiding leakage, etc. Advisors specifically have been striving to optimize alpha (given risk aversion) through good allocation and product selection during accumulation.

However, the opportunity for advisors to increase their “alpha” by helping employees squeeze out greater retirement income with the same assets during decumulation is rarely taken. While guaranteed lifetime income products can contribute to retirement readiness, no single product can translate accumulated assets into the maximum level of retirement income.

In our view, optimizing retirement readiness is not primarily a product solution, but rather a process solution. Morningstar summarized 2012 research into ways to increase retirement income and better meet retirees’ goals through what they call “Gamma.” Much of this increased Gamma can be generated now by advisors. Furthermore, Ernst & Young has validated LifeYield’s[1. LifeYield, LLC is a technology solutions provider that provides financial advisors with solutions for managing a household's multiple taxable and tax advantaged accounts. Paul Samuelson, Ph.D is its chief economist.] estimates of substantial increases in after-tax income with coordinated account management combined with coordinated sourcing of income. Essentially, retirement income maximization is achieved through a decumulation strategy that coordinates participants’ DC plan investments with their non-qualified accounts and de-cumulates them in a tax-efficient manner.

Coordinated Account and Income Source Management: Taking the Broad View of Accumulation and Decumulation

When assessing how we as an industry are doing in enhancing retirement readiness, we are not quite sure. Often, we have only a limited view into participants’ total retirement readiness picture since we are only looking at the DC assets in the current account. Obviously, looking at all the assets available to generate retirement income simultaneously is necessary. But optimizing retirement income when the assets are in a variety of locations is a daunting challenge for the participant, certainly, and often very difficult for the advisor. Furthermore, we tend to place most of the focus on the retirement income potential of the accumulated assets, and far less on the retirement income enhancement potential of an efficient decumulation strategy.

Coordinated account management occurs before and after retirement and focuses on locating the right assets in IRAs and taxable accounts to achieve higher after-tax returns. For DC plans, this may require an adjustment in the participant’s plan allocation, so that the overall household’s target asset allocation, across all of the accounts, meets the retiree’s overall risk tolerance.

Coordinated income sourcing begins when retiring participants construct their own retirement paycheck. In this process, advisors make annual recommendations of how much to withdraw from IRAs and brokerage accounts to fund retirement income, pay taxes and in some cases fund conversions to Roth accounts (to provide more capacity for tax-free accumulation). For many retirees in satisfactory health and with sufficient investment assets, there will be a recommendation to delay Social Security to significantly increase monthly payments (and reduce the burden on investment accounts). Of course, all recommendations depend on the retirees’ circumstances and preferences, and require sophisticated software for their calculation.

A Picture of a Household is Worth a Thousand Words of Explanation

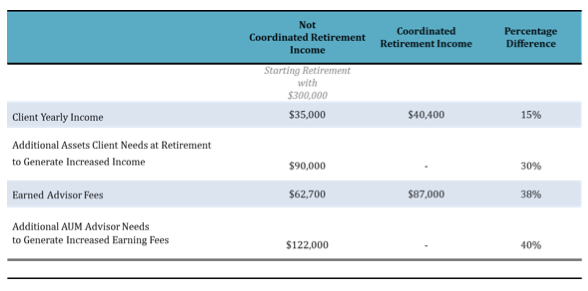

Let’s look at an example of a typical participant’s retirement assets at age 65. Combined total value of household for husband and wife starting retirement at age 65 with $300,000 in retirement assets:

• Qualified accounts (401ks & IRAs): $220,000

• Taxable accounts: $80,000

• Income before retirement: $77,000 (50% equity, 50% bonds)

• Retirement income needed: $35,000/year

• Increased Social Security payments reduce later withdrawals from accounts

• Roth Conversions increase capacity for tax free returns

• Income projections go up to age 95

• Delayed Social Security is financed by early withdrawals from brokerage account

With coordinated rather than conventional management[2. Defined by Ernst &Young as comparable asset allocation for both qualified and non-qualified accounts and pro-rata income distribution from each account.] this $300,000 can provide 15% more retirement income by age 95. To realize that additional income in retirement, the participant would have had to accumulate an additional $90,000 by age 65.

Morningstar translates the additional income into an equivalent amount of additional return each year — the Gamma described above. They estimate that 52 BPs come from optimal (tax-efficient) asset location (coordinated account management), 54 BPs from optimal retirement income sourcing, and 38 BPs from keeping the household allocation aligned to the target financial plan.

Coordinated account management and income sourcing provides retirees with more retirement income, but importantly, larger ongoing account balances through retirement. In this conservative example, the advisor would have realized an extra 38% in income off the same account. To generate that income, the advisor would have had to collect an additional $122,000 in assets.

Of course, leaving the money in an appropriate product is important but process has the biggest impact. Importantly, this process allows the client to keep the same products and the same total household asset allocation, by executing the plan the advisor has created. This process also provides a compelling argument for consolidating assets under one advisor while substantially reducing fees and complexity from the participant’s point of view.

Doing all of this manually is next to impossible. That’s one reason why it’s so rarely done. (To learn more about how this is done automatically for the advisor, go to http://www.lifeyield.com.)

In summary, applying a state-of-the-art decumulation strategy appears to be a win-win-win for the DC industry. The plan sponsor wins by improving retirement readiness, and the participant wins by receiving greater retirement income from the same asset levels. Additionally, the advisor wins by providing better service, adds value to his/her fees, increases advisor “alpha” and enhances his/her income off the same asset levels.

Paul Samuelson, the CIO and chief economist for LifeYield, holds a Ph.D. and an M.S.M. from the Massachusetts Institute of Technology. Warren Cormier is CEO of Boston Research Group, a leader in DC industry research.

Footnotes