The ERISA consultants at the Learning Center Resource Desk, which is available through Columbia Threadneedle Investments, regularly receive calls from financial advisors on a broad array of technical topics related to IRAs and qualified retirement plans. A recent call with an advisor in New York is representative of a common inquiry regarding controlled group rules. The advisor asked:

“Do the IRS’ controlled group rules apply to tax-exempt entities?”

- Yes, certain entities that are exempt from tax under Internal Revenue Code Section (IRC §) 501(a) are subject to a subsection of the controlled group rules pursuant to Treasury Regulation 1.414(c)-5. The controlled group rules, in general, require that all employees of commonly controlled entities be treated as employees of a single entity for various retirement plan qualification purposes.

- For this purpose, common control exists between an exempt organization and another organization if at least 80 percent of the directors or trustees of one organization are either “representatives” of, or are directly or indirectly “controlled” by, the other organization. (Please note there are separate rules that apply to church and qualified church-controlled organizations.)

- A trustee or director is treated as a representative of another exempt organization if he or she also is a trustee, director, agent, or employee of the other exempt organization.

- A trustee or director is controlled by another organization if the other organization has the general power to remove such trustee or director and designate a new trustee or director.

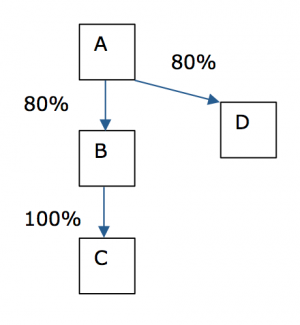

Example

- Tax-exempt organization A has the power to appoint at least 80% of the trustees of tax-exempt organization B.

- B owns all of the outstanding shares of corporation C, which is not a tax-exempt organization.

- A also controls at least 80% of the directors of tax-exempt organization D.

- Entities A, B, C, and D are treated as the same employer with respect to any plan maintained by A, B, C, or D.

Conclusion

Some may be surprised to learn there is a subsection of the IRS’ controlled group rules that apply specifically to tax-exempt entities. Determining whether a controlled group exists is important as the IRS will treat all employees of commonly controlled entities as employees of a single entity for various retirement plan qualification purposes.

The Learning Center Resource Desk is staffed by the Retirement Learning Center, LLC (RLC), a third-party industry consultant that is not affiliated with Columbia Threadneedle. Any information provided is for informational purposes only. It cannot be used for the purposes of avoiding penalties and taxes. Columbia Threadneedle does not provide tax or legal advice. Consumers consult with their tax advisor or attorney regarding their specific situation.

Information and opinions provided by third parties have been obtained from sources believed to be reliable, but accuracy and completeness cannot be guaranteed by Columbia Threadneedle.

Columbia Threadneedle Investments (Columbia Threadneedle) is the global brand name of the Columbia and Threadneedle group of companies.

©2016 Columbia Management Investment Advisers, LLC. Used with permission.