The ERISA consultants at the Learning Center Resource Desk, which is available through Columbia Threadneedle Investments, regularly receive calls from financial advisors on a broad array of technical topics related to IRAs and qualified retirement plans. A recent call with a financial advisor in Massachusetts is representative of a common question related to Roth IRA beneficiary options. The advisor asked:

“My client has a Roth IRA and named someone other than his spouse as the beneficiary. What are the beneficiary’s distribution options?”

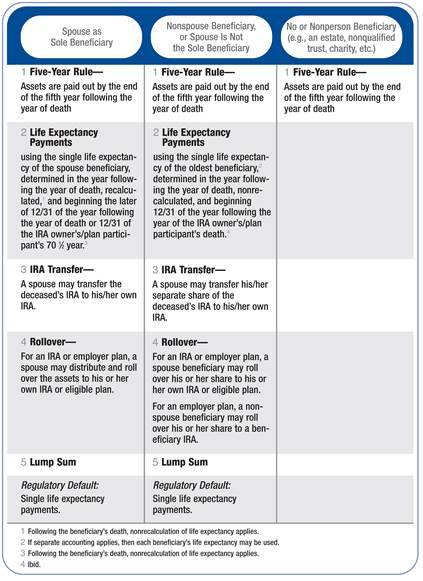

Highlights of Discussion

• It is important to check the Roth IRA plan agreement language for the availability of specific beneficiary options. The plan agreement may specify fewer options than what is allowed under Treasury regulations.

• The following table summarizes the distribution options available according to Treasury regulations. (Note: They are the same options that would apply to the beneficiary of a traditional IRA or qualified retirement plan if the IRA owner or plan participant died before the required beginning date for starting mandatory distributions.)

• Since the client who the financial advisor is inquiring about has named a nonspouse beneficiary on a Roth IRA, refer to the center column for potential distribution options. The beneficiary options would be the five-year rule, life expectancy payments or a lump-sum payment.

• The processes of recalculation or nonrecalculation of life expectancy become important for the beneficiary following the death of the IRA owner or plan participant because they affect the life expectancy figure used in distribution calculations. Regulations dictate which applies. Before death, the life expectancy figure used to calculate an IRA owner’s or plan participant’s required minimum distribution is always recalculated.

• Recalculation: life expectancy is redetermined each year by referring to the appropriate life expectancy table.

• Nonrecalculation: life expectancy is set in a particular year by referring to the appropriate life expectancy table, and the life expectancy factor is then reduced by one for each subsequent year.

• Separate accounting of multiple beneficiary shares allows each beneficiary to determine his or her distribution independently. If separate accounts are not established, or are not properly maintained, beneficiary distributions are determined based on the oldest beneficiary.

• Regarding the tax treatment of Roth IRA distributions for a beneficiary, contributory dollars are always distributed on a tax- and penalty-free basis. Conversion dollars are always distributed on a tax-free basis and, because the beneficiary has a penalty exception (death), they are penalty-free as well, regardless of the amount of time held. Any distributed earnings would come out penalty-free at any time, but if taken before the Roth IRA has existed for five years, would be subject to taxation until the five-year period has expired. The amount of time the Roth IRA was held by the deceased would count toward the five-year period for determining taxability (Treas. Reg. 1.408A-6, Q&A 7).

Conclusion

The rules that govern beneficiary distribution options are primarily found in IRC Sec. 401(a)(9)(B) and underlying Treasury regulations (Treas. Reg. 1.401(a)(9)). Plan agreement language may further restrict the available options, so it is always important to review the distribution section of the plan agreement for specific options.

The Learning Center Resource Desk is staffed by the Retirement Learning Center, LLC (RLC), a third-party industry consultant that is not affiliated with Columbia Threadneedle. Any information provided is for informational purposes only. It cannot be used for the purposes of avoiding penalties and taxes. Columbia Threadneedle does not provide tax or legal advice. Consumers consult with their tax advisor or attorney regarding their specific situation.

Information and opinions provided by third parties have been obtained from sources believed to be reliable, but accuracy and completeness cannot be guaranteed by Columbia Threadneedle.

Columbia Threadneedle Investments (Columbia Threadneedle) is the global brand name of the Columbia and Threadneedle group of companies.

© 2015 Columbia Management Investment Advisers, LLC. Used with permission.