I once spent a very uncomfortable period of time stuck in one of those carnival rides that, for brief periods of time, spins riders in a circle as the cab you are in also twirls. As uncomfortable as the ride was, the “stuck” part came while my cab was high in the air — and turned upside down. In no time at all, it was obvious that this extended “upside down” state wasn’t contemplated by those who designed the seating compartment (nor, apparently, had they considered that my companion would find it exciting to rock our stuck cab during our brief “internment”).

One of the comments you hear from time to time is that the tax incentives for 401(k)s are “upside down” — that is, they go primarily to those at higher income levels, those who perhaps don’t need the encouragement to save. And from a pure financial economics perspective, those who pay taxes at higher rates might reasonably be seen as receiving a greater benefit from the deferral of those taxes.

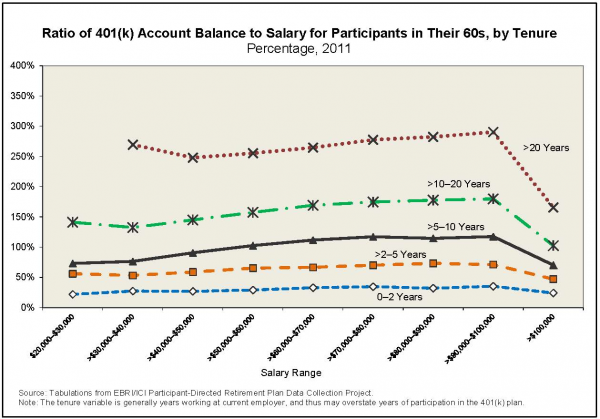

Indeed, if those “upside-down incentives” were the only forces at work, one might reasonably expect to find that the higher the individual’s salary, the higher the overall account balance would be, as a multiple of salary. However, drawing on the actual administrative data from the massive EBRI/ICI 401(k) database, and specifically focusing on workers in their 60s (broken down by tenure and salary), EBRI Research Director Jack VanDerhei has found that those ratios hold relatively steady. In fact, those ratios are relatively flat for salaries between $30,000 and $100,000, before dropping substantially for those with salaries in excess of $100,000. (See the accompanying chart; for a larger, more legible pdf of the chart, click here.)

In other words, while higher-income individuals have higher account balances, those balances are in rough proportion to their incomes. They are not “upside down.”

As retirement plan advisors are well aware, these programs are subject to a series of limits and nondiscrimination test requirements: the boundaries established by Code Sections 402(g) and 415(c), combined with the ADP and ACP nondiscrimination tests. Those plan constraints were, of course, specifically designed (and refined) over time to maintain a certain parity between highly compensated and non-highly compensated workers in the benefits available from these programs. The data suggest they are having exactly that impact.

So those who focus only on the incentives — and not also on the limits — are left “stuck” with only part of the answer.