To view a PDF version of this article, click here.

Fitness experts say that a strong core supports your whole body and a weak one can put you at risk for physical problems. The same holds true for a defined contribution plan’s investment lineup — and a participant’s investment portfolio. What’s at the core can make or break retirement outcomes.

Active investment strategies are essential to a strong core and a necessity in today’s challenging markets, which are more complex, volatile and short-term-focused than ever. To navigate conditions like these, your defined contribution clients need skilled active management that selects securities thoughtfully, chooses risks intentionally and focuses on long-term value rather than short-term market swings.

The Cost of Surprises

Following recent fee disclosure regulations, there has been a great deal of focus on the costs associated with retirement plans, and the response has been a noticeable shift to passive investments. While fees need to be transparent, properly disclosed and reasonable, it’s important to look at costs holistically. A passive-only core may lower explicit fees, but it may subject participants to potential damage, creating significant and unexpected costs during market downturns.

That’s because while an entirely passive core — whether at the plan lineup or participant portfolio level — may hold up well in continuously rising, efficient markets, it can actually weaken a participant’s outcome as volatility grows. Passive strategies take full market risk and thus follow the market’s short-term trends, upward or downward.

Lacking active risk management, a passive-only core subjects participants to the potential damage that increasing market volatility can do to their returns.

That danger is very real. Left unmanaged, volatility hinders the benefits of com- pounding and diminishes the rate at which investments can grow over time. For example, let’s say a participant has a $100,000 portfolio that drops 15% in value one month and rebounds 15% the next. While the average return is zero, the portfolio still loses value. That’s because while the 15% drop would have reduced the portfolio to $85,000, the 15% rebound would bring that $85,000 back to only $97,750. The $2,250 loss incurred is called “volatility drag,” and, over time, it can do irreparable damage to retirement outcomes.

There is similar concern in a severe market downturn. A passive core has no means of protecting capital, and as we saw in the global financial crisis of 2008, losses sustained in bear markets can be especially troublesome for investors nearing retirement. Yet passive investors don’t seem to understand the true meaning of taking full market risk. In a survey conducted by MFS, nearly two-thirds of investors thought their stock index funds were safer than the market.

A Strong Core Carries More Weight

Skilled active management can strengthen the core of a plan lineup and a participant portfolio, working alongside passive or on its own. That’s because it has the research capabilities and active security selection to add value when the indices are inefficient, and uses active risk management to navigate volatility and changing market cycles effectively. “Activating the core” can broaden investment opportunities for your defined contribution clients while seeking to minimize losses along the way.

Turning Market Challenges into Opportunities

As the capital markets become more interrelated and companies operate more globally, the best investment opportunities could be anywhere in the world. To find them for defined contribution clients, active managers can immerse their analysts in local markets worldwide and use integrated research capabilities to evaluate an enormous amount of global information and develop the best of their investment ideas.

Active managers can also look past the markets’ growing short-term focus, which runs counter to defined contribution plan participants’ long-term objectives. By focusing on solid fundamentals, active managers pursue long-term value and sustainable returns, rather than trying to invest on short-term price swings driven by news flow and analyst earnings estimates. They can also use market “short-termism” as an opportunity.

While the prices of securities tend to move in concert over short time frames, over longer periods, active managers can find a broader range of returns (“dispersion”) and distinguish between the best and worst companies. Active managers who are patient enough to hold securities for three to five years or more can potentially provide the type of long-term value that participants need to improve their retirement outcomes.

Building Strength Through Active Risk Management

In a human body, a strong core protects against injuries. In a participant portfolio or plan lineup, a core made stronger through active risk management attempts to minimize losses in a market downturn. Unlike passive management, which takes full market risk, active management can budget risk thoughtfully and try to avoid the highest-risk companies and segments of the market.

That’s especially important during “bubbles” — technology in the 1990s and financials in 2008 — when having full market exposure can be devastating to a retirement portfolio. For defined contribution investors, the abilityto minimize losses in market downturns is just as important as, if not more so than, pursuing gains in strong markets.

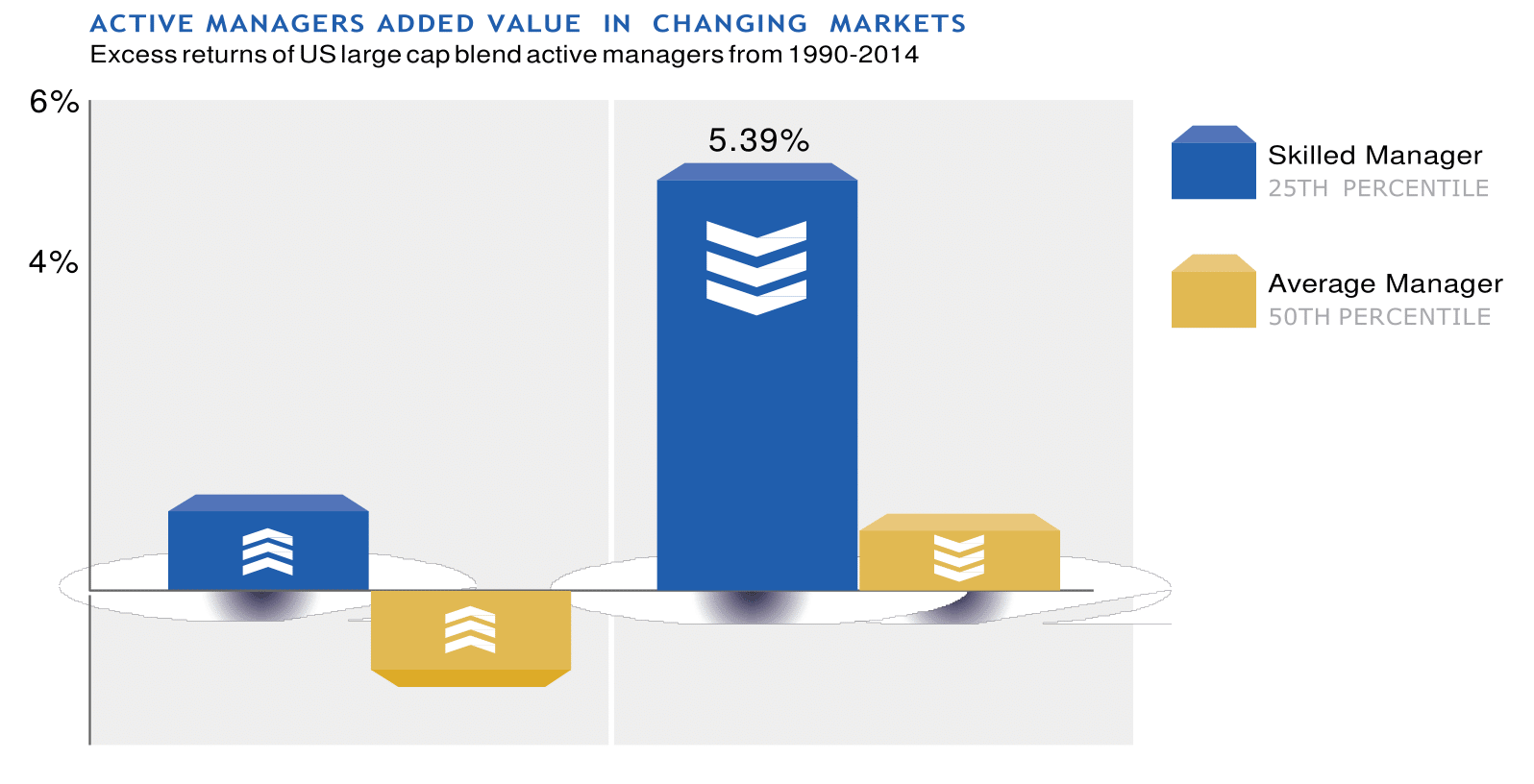

The chart above illustrates how active management supports a portfolio through changing market conditions. Specifically, we looked at the S&P 500 over the past 25 years and compared the performance of what we define as skilled active managers (top 25%) and average active managers (top 50%) when markets both rose and fell in a given year. We found that while active managers in general added value in down markets, skilled active managers added value in both types of markets.

A strong core uses different muscle groups to help protect the rest of the body. For your defined contribution clients — at the portfolio or plan level — a strong core can be built in different ways using a variety of investment strategies. Because that core is the foundation that must support a successful retirement outcome, however, it’s important to keep at least part of it highly skilled and very active.

Ryan Mullen is MFS’ Senior Managing Director and Head of Defined contribution Investments.

Ryan Mullen’s comments, opinions and analyses are for informational purposes only and should not be considered investment advice or a recommendation to invest in any security or to adopt any investment strategy. Comments, opinions and analyses are rendered as of the date given and may change without notice due to market conditions and other factors. This material is not intended as a complete analysis of every material fact regarding any market, industry, investment or strategy.

32997.1

This article originally appeared in the June 2015 Special Outcomes Issue of NAPA Net the Magazine.