To view a PDF version of this article, click here.

For decades, the retirement industry has concentrated on improving the retirement readiness of American workers through financial literacy education. Workers receive a steady stream of logic-based data and terminology, tons of paperwork (literal or online), and quarterly statements.

Yet, despite the best intentions of many people, industries and companies, the annual household savings rate hovers at 3.8% and three-quarters of Americans do not have enough saved to cover six months of living expenses.

So, why is the savings picture still so bleak? Unfortunately, the effort to promote savings focuses almost exclusively on appealing to the brain’s frontal cortex. Retirement plan providers pay scant attention to eliciting an emotional response that can build confidence and retirement preparedness.

Behavioral Design Provides Relevant Framework

Plan advisors who work with participants know that getting people to overcome fear and inertia is a huge first step in retirement planning. To help understand this process more fully, academic researchers are now looking closely at the complex innate mechanisms by which people make decisions or pursue certain behaviors.

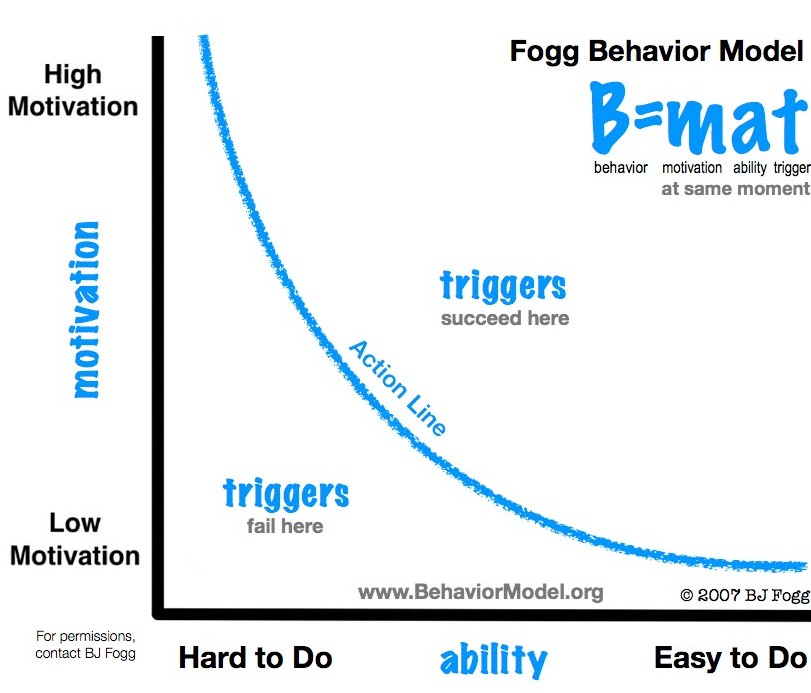

Stanford University Professor BJ Fogg's Behavior Model (FBM) suggests that for a person to perform a desired behavior, he or she must be sufficiently motivated, have the ability to perform the behavior, and be triggered to perform the behavior.

Fogg believes that if you motivate people to complete easy-to-do activities (the lower right), you can use triggers to guide them along an “activation threshold” and tackle harder-to-complete tasks (such as saving 10 % of their salaries).

The issue we work to address in many enrollment meetings is motivation. Unfortunately motivation alone is variable. (Someone may have just received bad news about his or her cell phone bill as an example.) Making something easy to do is engineered into the solution — and is not variable. (Sound like auto enrollment?)

My take on why this approach works brings in another concept. If people can tackle a very simple task, they gain a greater sense of what psychologist Albert Bandura called self-efficacy — the confidence in the ability to exert control over one’s own motivation, behavior and social environment. Put another way, if people complete one small task, they come to believe in their ability to complete more difficult tasks.

Improved Outcomes Relies on Building Confidence

Today, several industry innovators — vWise, Commonwealth Financial and MassMutual, as examples — are using a variety of these behavioral principles to help workers take a more active role in financial planning.

To complement the traditional employee education methods, vWise, Inc. a Southern California software solutions provider, is leading the development of an intriguing participant engagement platform that implicitly employs FBM principles. vWise’s software, SmartPlan, uses small, incremental triggers to get an employee to take specific action: watch a 90-second video, select a contribution amount, or choose or make investment adjustments — preferably during a single online session that occurs where and when the employee dictates.

What’s unique about SmartPlan is that it’s an interactive experience designed to provide motivation, ability and triggers to average American investors in a “just-in-time” sequence.

The outcomes-based philosophy behind SmartPlan asserts that financial literacy levels do not predict how actively employees engage with their plan. Instead, the software provides workers with motivating triggers to enter information that generates interest and excitement about their own personal outcomes, and thereby encourages them to join their workplace retirement plan and begin investing.

For Jeremy Katz, a financial advisor with AXA Advisors, SmartPlan helps employees make good decisions. "By viewing short one- or two-minute video vignettes, employees uncover personally relevant information that leads them to take a small action, whereas a typical plan website requires them to click through many more pages that communicate on a far more generic, and to my mind less effective level," adds Katz.

Small Steps and Accomplishments Create Action

Behavioral design works best when difficult decisions follow a continuum of small, easy accomplishments. Commonwealth Financial Network recently implemented a simple seven-question, multiple choice, survey for use at the beginning of retirement plan enrollment meetings. The survey was designed to accomplish two things:

- Build a sense of accomplishment — self efficacy — at the outset of the meeting by having employees complete an easy-to-do task.

- Elicit personal responses from employees regarding how they feel about investing for retirement with phrases such as Are you confident? Are you comfortable? (Employees may not intuitively understand their risk tolerance. Many people are able to express how they feel about an issue, particularly when prompted with multiple-choice answers.)

The survey uses behavioral design and adult learning theory to establish a diverse employee group confidence baseline. Then, the meeting design uses a series of effective “triggers” to move employees up along the activation threshold to motivate them to enroll in the plan or add to their savings.

“Making the presentation personal to each participant is absolutely the key to getting them to engage,” explains John Higgins, a Wealth Manager and Retirement Plan Consultant with Commonwealth. “Plan sponsors get a surge in interest in the plan when employees use this personalized approach.”

Investing is Both Rational and Emotional

While many people agree that investment decisions are best made based on reason, emotions play a huge role in either helping or hurting an otherwise sound investment or savings strategy.

The Society for Grownups, developed by MassMutual and IDEO, operates as a Master’s Program for Adulthood, is trying to bridge the gap between the head and heart to improve financial well-being.

Not surprisingly, the Society primarily targets Millennials, a group that is often unfairly accused of putting off financial planning. By offering small, in person salons on subjects such as Investing & Fine Wine, the Society for Grownups draws similarities between the familiar and unfamiliar, the emotional and logical, and in so doing seeks to draw a distinction between the comfortable and unknown. Their approach provides for a super easy and enjoyable way to discuss and discover the world of finance. (Head over to societyofgrownups.com for some awesome examples of approaching the Millennial marketplace.)

Improving Outcomes

Behavioral design follows a model that invites — rather than demands — a user's active participation and engagement using three key principles:

- Soliciting real-world information about an employee’s personal situation and preferences lessens common motivational frustrations about financial education and plan engagement.

- “Just-in-time" bite-sized delivery of information helps improve the user’s confidence level — a far better predictor of action than his or her level of financial literacy.

- Specific triggers, properly sequenced along the ‘activation threshold,’ can greatly improve the motivation (and self-efficacy) and guide them to taking desired action.

Retirement plan providers and advisors have long looked for viable ways to crack the code for encouraging greater levels of engagement and contributions to their plans. These innovative behavior-based education models show great promise. The tide for participant outcomes finally could be turning.

Sheri Fitts is Founder of ShoeFitts Marketing, a nationally based financial services consulting firm based in Portland, Ore.

This article originally appeared in the June 2015 Special Outcomes Issue of NAPA Net the Magazine.