The ERISA consultants at the Learning Center Resource Desk, which is available through Columbia Threadneedle Investments, regularly receive calls from financial advisors on a broad array of technical topics related to IRAs and qualified retirement plans. A recent call with an advisor in Tennessee is representative of a common inquiry involving the IRS rules regarding controlled groups. The advisor asked:

“What is a brother-sister controlled group of businesses, and why is it important to know if a controlled group exists?”

Highlights of Discussion

- There are three types of controlled groups: parent-subsidiary; brother-sister; and a combination of the two.

- It is important to determine whether a group of businesses is a controlled group because the IRS requires that all employees of companies in a controlled group be treated as employed by a single employer for qualification requirements of various Internal Revenue Code Sections, including Sections:

- 401 (general qualifications);

- 401 (general qualifications);

- 408(k) (simplified employee pension (SEP) plans);

- 408(p) (saving incentive match plan for employees (SIMPLE) plans);

- 410 (minimum participation standards);

- 411 (minimum vesting standards);

- 415 (limits on benefits and contributions); and

- 416 (top-heavy determination).

- 401 (general qualifications);

- A controlled group determination should only be made by a competent legal professional.

- The IRS defines a controlled group of businesses in Code Sections 414(b) and (c) as a combination of two or more businesses that are under common control within the meaning of Section 1563(a). Businesses include proprietorships, partnerships and corporations. A brother-sister controlled group exists between two or more businesses when five or fewer common owners (individuals, estates or trusts) have both a controlling interest in the businesses and effective control.

- Controlling interest is defined as five or fewer owners of the group of businesses together owning at least 80% of the businesses (see Treasury Regulation 1.414(c)-2(b)(2)).

- Effective control means the same five or fewer owners own more than 50% of the businesses (see Treasury Regulation 1.414(c)-2(c)(2)). There is a twist to determining ownership for the effective control test. An individual’s ownership is considered only to the extent he or she has that same level of ownership interest in each of the organizations in the group.

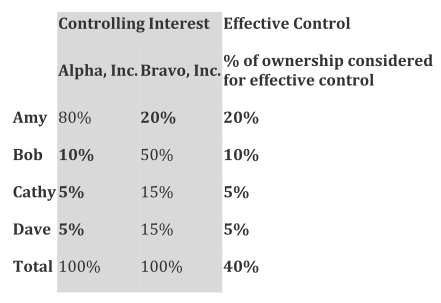

Example

- In this example, the four shareholders have a controlling interest because together they own 80% or more of the group of businesses. (They own 100% of both Alpha and Bravo.) However, combined, they do not have effective control because they do not own more than 50% of the businesses, taking into account only the identical level of ownership each has in the businesses as demonstrated above.

Conclusion

The IRS controlled group rules affect employer-sponsored retirement plans in a number of ways. To start, employees of a controlled group of businesses are viewed as employed by one entity. This has implications for applying qualification requirements of the tax code. Because an accurate controlled group determination is critical, businesses should rely on their legal advisors to conduct such analyses.

The Learning Center Resource Desk is staffed by the Retirement Learning Center, LLC (RLC), a third-party industry consultant that is not affiliated with Columbia Threadneedle. Any information provided is for informational purposes only. It cannot be used for the purposes of avoiding penalties and taxes. Columbia Threadneedle does not provide tax or legal advice. Consumers consult with their tax advisor or attorney regarding their specific situation.

Information and opinions provided by third parties have been obtained from sources believed to be reliable, but accuracy and completeness cannot be guaranteed by Columbia Threadneedle.

Columbia Threadneedle Investments (Columbia Threadneedle) is the global brand name of the Columbia and Threadneedle group of companies.

© 2015 Columbia Management Investment Advisers, LLC. Used with permission.