There’s been a lot of rumbling on and around Capitol Hill about a potential shift to Roth contributions for 401(k) plans as part of tax reform. So, how might that weigh on – or boost – retirement savings?

While the ultimate answer depends on a huge (and as yet) unknown variable – how workers would respond to a mandatory change – Jack VanDerhei, Research Director at the nonpartisan Employee Benefit Research Institute (EBRI), has modeled the potential impact on retirement savings shortfalls under a variety of scenarios.

The bottom line? The impact of a switch to Roth is less than one might think – and it could even close the nation’s retirement savings shortfall.

Previous Roth Research

In a presentation to EBRI’s Research Committee this week, VanDerhei noted that previous EBRI surveys had recently been cited by a media anxious to anticipate the prospects of a Roth switch. He cited the 2011 Retirement Confidence Survey, in which individuals were asked about the importance of their ability to deduct their retirement contributions as a factor in their decision to save. More than 6 in 10 (61.5%) said that was “very important,” while another 27.8% said it was “somewhat important.” However, VanDerhei cautioned that this was not specifically focused on the Roth issue on the table now, specifically that there was no mention of the potential for tax-free distributions at a later point in time.

Moreover, another question from that same survey that hasn’t been cited was that, when asked how they would respond to no longer being able to deduct their contributions, more than half (56.2%) said they would continue to save what they do now. Indeed, just over 17% said they would increase the amount they are saving now, though one in five said they would reduce their contributions, and just under 5% said they would stop saving for retirement altogether.

The subject of employee contribution deductibility was also part of the 2012 Retirement Confidence Survey, though again it was in a slightly different context. Still, that survey found that lower income workers (those making $15,000 to $25,000) were far more likely to say they would reduce the amount they would save and to cite the importance of deductibility in their decision to save. This might be viewed as somewhat ironic since members of this group, because they are subject to lower tax rates, arguably garner less benefit than the higher-paid workers who did not respond as negatively to the proposal.

VanDerhei also acknowledged a 2015 study by John Beshears, James J. Choi, David Laibson and Brigitte C. Madrian that focused on 11 companies that added a Roth contribution option to their existing 401(k) plan between 2006 and 2010. That study found no decrease in employee contributions because of the introduction of a Roth feature – although, as VanDerhei explained, a lack of response to the addition of a voluntary choice really has no bearing on how individuals might respond to the imposition of Roth tax treatment.

Switch ‘Plots’

Despite all the talk and concerns about a potential shift to Roth, with no specific proposal yet on the table, VanDerhei looked to consider the impact of a complete switch to Roth contributions in all 401(k) plans, effective in 2018.

Lacking any data upon which to extrapolate worker response to this Roth change, VanDerhei modeled assumptions in which all participants who have at least one more year of participation:

- Left contributions unchanged

- Reduced contributions 5%

- Reduced contributions 10%

- Reduced contributions 15%

- Reduced contributions 20%

- Reduced contributions 25%

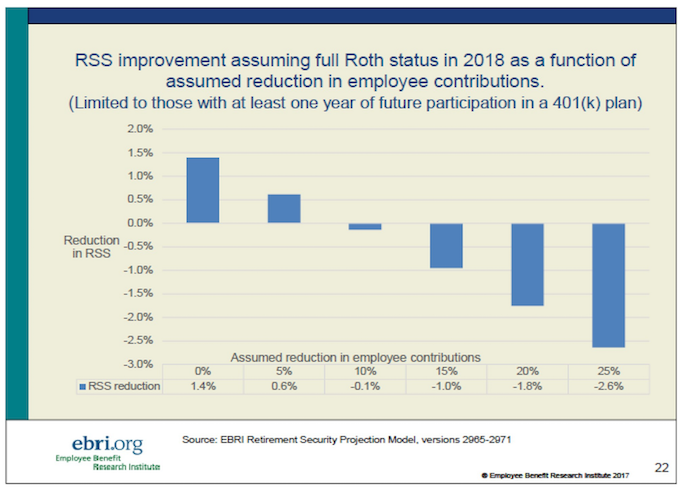

Based on this analysis, VanDerhei reported that when no reduction in contributions is assumed, the aggregate retirement savings shortfall (for those who have at least one more year of participation) shrinks, by 1.4%. Similarly, even if a reduction in contributions of 5% is assumed, the retirement savings shortfall is reduced, by 0.6%. (See chart.) Said another way, at least for that range of assumptions (including the assumption that today’s tax rates hold), those who are projected to run short of money in retirement are better off with a Roth account.

‘Break’ Points

As it turns out, the break-even point in terms of where the tax advantages of Roth at the back end in retirement largely equal out the advantages of deferral at the front end lies at a 9.1% reduction in contributions. Beyond that point, the Roth option (and the assumed reduction in retirement savings) worsens the retirement savings shortfall – though even assuming a 25% reduction, the shortfall deepens by a mere 2.6%.

Not included in this particular analysis, but on the radar for future development, is how the switch to Roth might affect the accumulations of participants, and how different tax rates assumption in the future might change the results.

Additionally, EBRI plans to launch a consumer survey this month to ascertain employee reactions to a Roth switch.

The bottom line? A switch to Roth – even a 100% switch – could have a positive impact on retirement savings shortfalls, at least assuming workers don’t respond too negatively.

And that, for now, remains a key question.