Employers in California, Illinois and Oregon, three of the first states to launch programs to help private sector workers save for retirement, were still creating new plans in 2020 and were shedding existing plans at rates slower than or largely comparable to the national average, according to a newly updated analysis of Form 5500 data.

Employers in California, Illinois and Oregon, three of the first states to launch programs to help private sector workers save for retirement, were still creating new plans in 2020 and were shedding existing plans at rates slower than or largely comparable to the national average, according to a newly updated analysis of Form 5500 data.

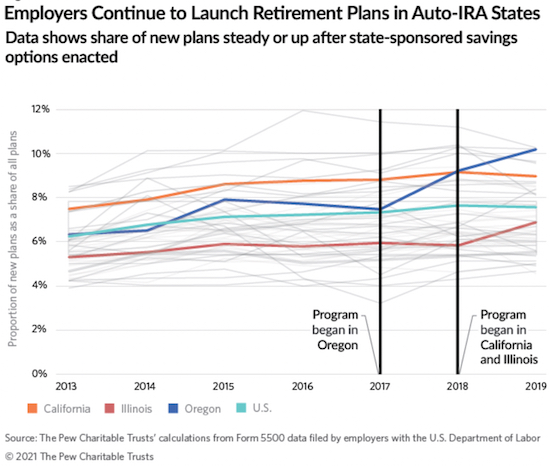

A June 2021 Pew Charitable Trusts analysis of data from Form 5500 annual filings from 2013 to 2019 suggested that in states which have created auto-IRA programs, employers with plans continued to offer them and businesses without plans were adopting new ones at rates similar to before the state auto-IRA options were available.

Newly updated data for 2020 shows comparable results, Pew reported July 25, despite the impact of COVID-19 on the economy more broadly. While the pandemic’s economic shifts may make some analysis more difficult, Pew notes, individual state numbers can still be viewed in comparison with the national average.

Earlier research suggested that auto-IRAs would complement, not compete with, the private retirement plan market. In 2017, Pew published the results of a national survey of small-business owners and benefits managers that detailed their views of hypothetical auto-IRA programs. Among those whose companies had retirement plans, only 13% said they would drop theirs and enroll in such a program if one was available in their state. Among small employers without plans, 51% said they would start their own plan rather than enroll workers in the state-facilitated program.

The updated analysis of Form 5500 filings is consistent with that research, Pew reports. California and Oregon still have higher rates of retirement plan creation than the national average, and California’s share of new plans compared to existing ones in 2020 remains among the highest in the country. Illinois, meanwhile, has had a lower share of new to existing plans than the national average since 2013, and that has not changed. In all three states with auto-IRAs, the rate of introduction of new plans, as a share of existing plans, is higher than before these states introduced the savings programs.