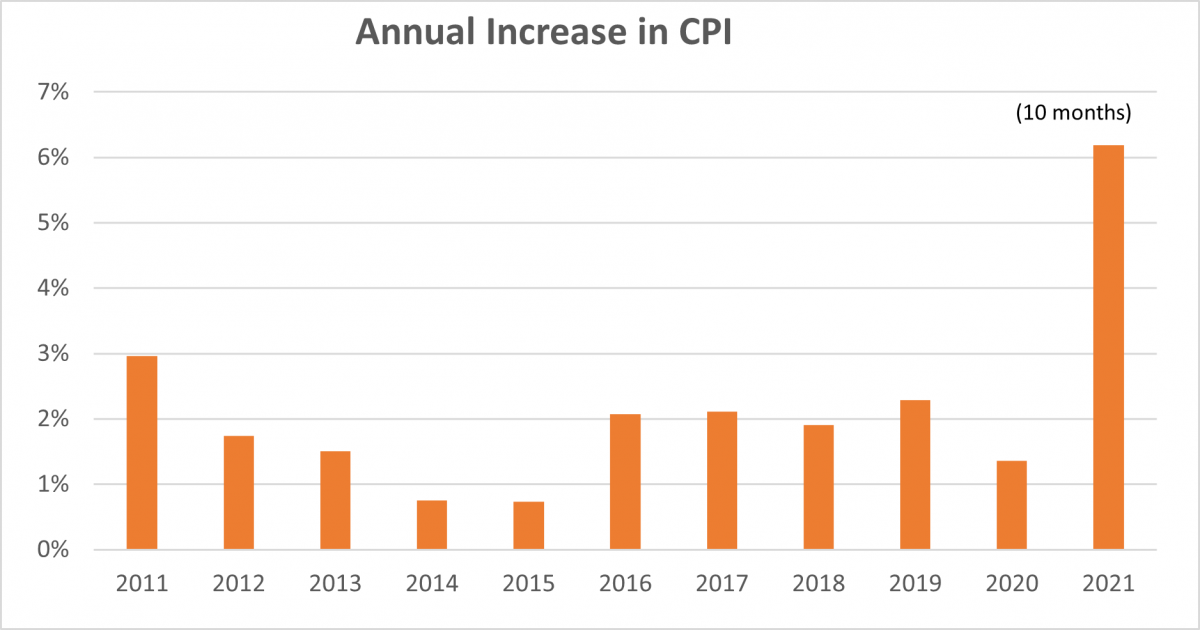

The Consumer Price Index (CPI) has risen steadily throughout 2021, with prices in October 2021 6.2% higher than at the beginning of the year.

The Consumer Price Index (CPI) has risen steadily throughout 2021, with prices in October 2021 6.2% higher than at the beginning of the year.

We have all been pretty much ignoring inflation as a retirement savings/income risk for some time. Understandably, since inflation for the last decade has averaged less than 2%.

However, with 2021 inflation already this high—and the prospect of more inflation ahead—we can no longer afford to do so.

Inflation’s Effect on Retirement Security

An increase in the CPI means a reduction in the buying power of a (nominal) dollar. So, if an individual’s pension could buy $1,000 in goods and services at the beginning of 2021, it only buys $940 of goods and services now.

Obviously, when we talk about “retirement income” or “retirement security,” we are not talking (literally) about how much money (in nominal dollars) an individual is getting, e.g., from a defined benefit plan annuity. What we’re actually talking about is how much food, gas, utilities, housing, medical services, etc., the individual can buy with that income.

(Chart source: Minneapolis Federal Reserve; DOL Bureau of Labor Statistics)

(Chart source: Minneapolis Federal Reserve; DOL Bureau of Labor Statistics)

Based on 2021 experience, retirement savers need to start taking inflation into account in their calculations.

Inflation Directly Affects Annuitants

Those directly affected by inflation are (1) defined benefit plan annuitants and (2) defined contribution plan participants who have bought (either in the plan or outside of it) an annuity. (Our focus in this article is on inflation and retirement policy. More broadly, inflation will affect investments (retirement and non-retirement) in the stock and (especially) bond markets.)

The effect of inflation on these two types of retirees differs. For DB participants, all inflation (including expected inflation) represents a loss. For annuitizing DC participants, on the other hand, the real culprit is unexpected inflation. As a general matter, expected inflation can be assumed to be taken into account in the interest rates used to price any annuity they purchase.

For DC Participants Who Have Not Annuitized, the Effect of Inflation Is Less Clear

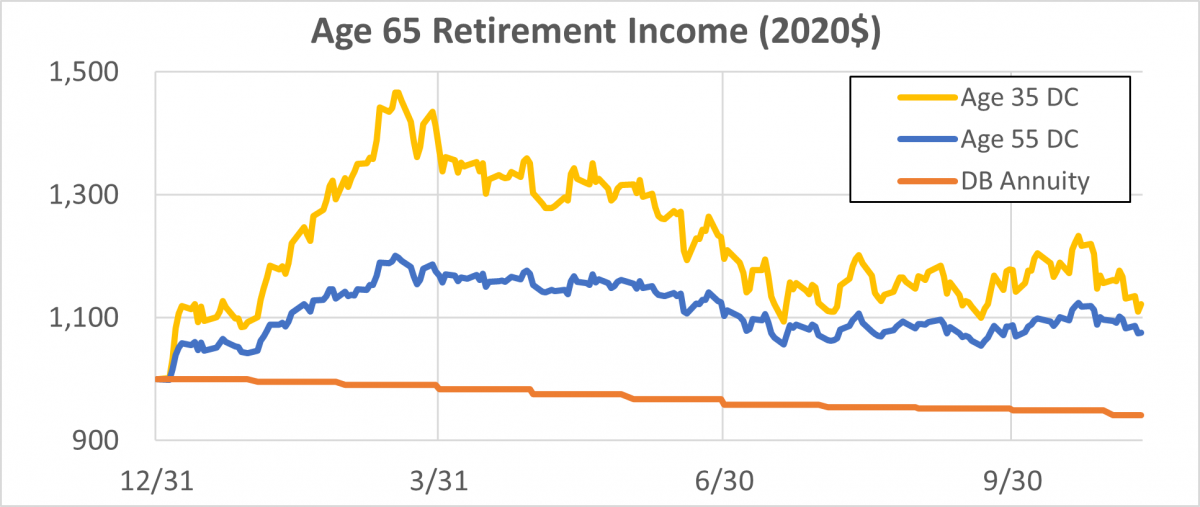

For 2021, thus far, DC participants who have not annuitized have generally, and notwithstanding the spike in inflation, done well. The S&P 500 is up over 25%. And the (at least partly inflation-driven) increase in interest rates means that the cost of retirement income (e.g., the price of a life annuity) has gone down.

We tracked the projected age 65 retirement income of two example DC participants (ages 35 and 55) invested in a standard, age appropriate target date fund. Each participant, as of the beginning of the year, would have been able to buy a $1,000 per month annuity with her account balance. Here’s the chart for mid-October 2021, adjusted for inflation (these numbers are in 2020 dollars, i.e., after adjusting for inflation), with the “performance” of a DB annuity included for comparison:

(Source: October Three, LLC.)

As the chart makes clear, both the age 35 and the age 55 DC (non-annuitizing) participants have done well this year. Currently, they are able to buy (in 2020 dollars) significantly more retirement income than they could at the beginning of the year.

Compare the performance of the DB participant’s annuity, which lost value (because of inflation) against its beginning of the year value of $1,000 (again, in 2020 dollars). An identical fate would have befallen our DC participants if they had annuitized at the beginning of the year.

Annuitization Triggers Inflation Risk

What should be obvious from the foregoing is that annuitization in a DC plan/for a DC participant, unless what is involved is a (very expensive and hard to find) inflation-protected annuity, triggers inflation risk.

In a world of steady, predictable 2% inflation, that risk could be ignored. And the advantages of annuities have been touted as a hedge against longevity and interest rate risks. In the current context, however, with the possibility of significant future inflation, annuitization is especially exposed to this risk.

That possibility should cause us to do two things:

- rethink how we communicate to participants about DC retirement income and retirement income risk; and

- consider (e.g., as a fund menu option) investments that are explicitly designed to hedge that risk.

What Can We Do to Help DC Participants Deal With Inflation?

DOL mandated lifetime income disclosure: The Department of Labor’s (DOL) lifetime income disclosure rule will, starting in 2022, require DC plan sponsors to provide participants with information about how much income their DC account balance will buy, pursuant to a uniform set of assumptions. Those assumptions include an interest/discount rate and (assumed) mortality. There is no inflation assumption.

DOL considered addressing the issue of inflation, noting that “even with a low inflation rate, the purchasing power of a fixed nominal income stream can easily be cut in half over the remaining lifespan of the typical retiree.” It solicited comments on whether, in place of 10-year Treasury rates, it should use the 10-year Treasury Inflation-Protected Securities (TIPS) rate.

Just for comparison, currently (as of Nov, 10, 2021) the yield on (“regular”) 10-Year Treasuries is 1.46%. The yield on 10-Year TIPS is -1.17%. (Just to be clear, the yield on TIPS—that is, interest reduced for expected inflation—is negative.) Using a simplified 20-year mortality assumption, a participant with $100,000 in his account can generate income of about $480 a month using the current 10-Year Treasury yield, but only about $370 a month using the TIPS yield—a 23% reduction in initial retirement income.

In this context, I would make two policy points regarding lifetime income disclosure. First, using TIPS in the lifetime income calculation introduces a speculative element, while for retirement income (as distinct from retirement investment), what matters in the end is actual inflation, not inflation expectations.

Second, how to introduce a CPI adjustment into a lifetime income disclosure is something of a challenge. Leaving it to the participant to intuit or guess at this effect is likely to leave some (perhaps many) individuals clueless. Probably the simplest “hack” here would be to first provide numbers in nominal dollars (as currently), and then, under a separate heading—labeled, say, “Adjustment for inflation”—provide those same numbers, e.g., for 2022, in 2021 dollars.

Participant education about inflation: In addition, DC plan sponsors may want to offer more general education about inflation’s effects on retirement income.

Inflation hedges in the fund menu: Finally, sponsors should consider offering inflation-hedging options in the fund menu and including inflation-hedging assets in the plan’s default target date fund, especially where annuitization is being encouraged.

It turns out that in addition to asset performance, interest rates and mortality/longevity, participants face a very real fourth risk: loss of retirement income buying power to inflation. One vexing aspect of this wrinkle is that the vehicles used to deliver a level stream of nominal income—annuities and bonds—are precisely the same vehicles that are particularly vulnerable to inflation risk.

Let’s do something about this now—especially as we focus on DC lifetime income solutions. There is still time to inform participants about this risk and provide them with options to do something about it.

Michael P. Barry is a senior consultant at October Three and President of O3 Plan Advisory Services LLC, which provides retirement plan regulatory analysis targeted at plan sponsors and those who provide services to them.

Opinions expressed are those of the author, and do not necessarily reflect the views of NAPA or its members.