After weeks of anticipation, the 5th Circuit Court of Appeals finally issued its mandate vacating the Labor Department’s fiduciary rule June 21.

The industry had been anxiously waiting as one key deadline, and then another, came and went. Just two weeks ago, the victorious plaintiffs in the 5th Circuit case asked the court to put the rule out of its collective “misery.” In a letter to the 5th Circuit, counsel for the plaintiffs noted that that court’s March 15 ruling vacating the fiduciary rule contained a docket entry noting that the mandate issue date would be May 7, 2018.

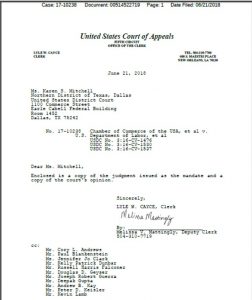

The Mandate

The mandate was contained in a 70-page document, but only a few pages were new – a cover memo that ran two pages, and the final judgment. which not only spoke to the disposition of the case (“This cause was considered on the record on appeal and was argued by counsel. It is ordered and adjudged that the judgment of the District Court is reversed, and vacate the Fiduciary Rule in toto.”), but also contained an order that the Labor Department “pay to appellants the costs on appeal to be taxed by the Clerk of this Court.” Most of the document was a copy of the March 15 decision.

June 13 had been widely cited as the last day the Department of Labor could appeal to the U.S. Supreme Court the 5th Circuit’s ruling vacating the fiduciary rule. That day passed without action – not that it came as a complete surprise that the DOL did not seek a review by the high court. The AARP and three states had attempted in separate motions to intervene in the litigation, citing the DOL’s lack of action to appeal the case, but those efforts were soundly rejected by the 5th Circuit – twice.

What Next?

What Next?

While the 5th Circuit’s decision has the effect of eliminating the requirements of the fiduciary rule, it also does away with the Best Interest Contract (BIC) Exemption, which provided a means for advisors to provide advice as an ERISA fiduciary and still receive commissions, in that it varies based on the advisor’s recommendation. So now the prevailing wisdom is that the DOL fiduciary rule, as it largely existed, is now dead and the old five-part test from 1975 comes back to life, which could be a problem for firms already operating under the new rule – which had been in place for nearly a year.

Also, remember that on May 7 the DOL issued Field Assistance Bulletin 2018-02 announcing that it was extending until further notice its temporary enforcement policy relating to its rule defining who is a fiduciary and the associated prohibited transaction exemptions.

The fiduciary regulation’s demise notwithstanding, the FAB is important because, even though the BIC Exemption has been set aside along with the rest of the rule, what the FAB essentially does is to provide for non-enforcement where the impartial conduct standards set forth in the BIC Exemption – which was in the fiduciary rule – are satisfied. Since the BIC Exemption was the only “clearly applicable” exemption for IRA rollovers, it contains the most reliable guidance we have on what the DOL thinks “best interest” means in the context of a rollover recommendation, according to Drinker Biddle & Reath’s Fred Reish and Joshua Waldbeser.

So, at least until – or if – the Labor Department updates that FAB, the fiduciary rule’s spirit of “best interest” lives on.