In 2020, the first quarter’s COVID-19-driven bear market led to losses for all target date vintages, and near-retirement investors withdrew funds. Despite diversified portfolios, investors expecting to retire in the year 2020, lost more than 17% on average in the 2020 vintages. Individuals expected to retire in 40 years (2060 funds) lost 31%—which is a minor improvement versus U.S. equities, which fell 33%, and global equities, which declined 32%, according to the firm’s data. Even though the market experienced a V-shaped recovery in a short period of time, the combination of the ubiquitous nature of target date funds mixed with the propensity for employees in certain demographic ranges to make rash investment decisions lays bare the need for employers and plan fiduciaries to better understand exactly what it is that they are serving up to their employees.

In 2020, the first quarter’s COVID-19-driven bear market led to losses for all target date vintages, and near-retirement investors withdrew funds. Despite diversified portfolios, investors expecting to retire in the year 2020, lost more than 17% on average in the 2020 vintages. Individuals expected to retire in 40 years (2060 funds) lost 31%—which is a minor improvement versus U.S. equities, which fell 33%, and global equities, which declined 32%, according to the firm’s data. Even though the market experienced a V-shaped recovery in a short period of time, the combination of the ubiquitous nature of target date funds mixed with the propensity for employees in certain demographic ranges to make rash investment decisions lays bare the need for employers and plan fiduciaries to better understand exactly what it is that they are serving up to their employees.

Utilizing over 27 million data points on over 150,000 different investments, the proprietary LeafHouse Grade Point Average (LeafHouse GPA®) algorithm and technology evaluates funds by incorporating performance, risk/reward, fees, and other qualitative/quantitative measurements. During Q1 of 2020, the market volatility increased due to Coronavirus uncertainty and oil price volatility. This shock to the system can refocus the attention of participants on their portfolio risk and downside exposure. As a prudent investment fiduciary, we looked at the volatility and downside protection of active, passive, and blend target date suites to identify how each was affected during this unprecedented market event.

Target Dates Are Defined as Active, Passive and Blend

Something that often gets overlooked in this paradigm is the glide path design of each different category of target date funds. Active target dates are managed to outperform each asset class benchmark through investing in either individual securities or a fund-of-funds. Passive target dates are constructed using index funds. Blend target date funds use a combination of both. Though passive and blend target date suites are constructed using indexes and are not utilizing “active” management in the traditional sense of the word.

The term “passive” when describing a target date suite is somewhat of a misnomer. No target date strategy is fundamentally “passive.” All target date funds engage in active decision-making to create and manage their glide paths. Each glide path takes active capital market assumptions in determining an optimum asset allocation across each vintage. When the industry refers to a passive target date suite the only things that should be considered “passive” are the underlying strategies that are being used.

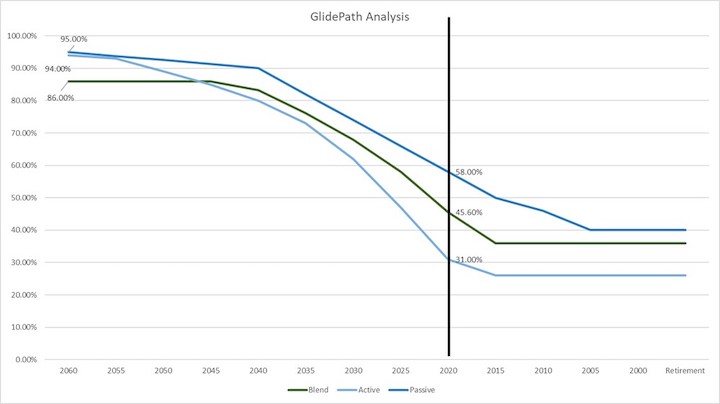

In the accompanying chart, notice the difference in equity exposure at the 2020 mark, which is retirement vintage for this year. The active reflects a 31% equity allocation, the blend allocates 45.60% to equity, and the passive invests in 58%. Each glide path should be researched and analyzed to provide confidence to plan sponsors and participants that the selection made for their plan is appropriate. If plan demographics point to a risk averse pool of investors, the lower cost, index option may not be the proper choice, considering the higher equity exposure near retirement.

Underlying Strategy Analysis is a Key Component of Determining Suitability of Any Target Date

At LeafHouse Financial, we run each underlying fund within the glide path and score it using our LeafHouse GPA® algorithm. This methodology helps us to identify if a fund family is using an underperforming fund when they may have a strategy within the same asset class that performs better. We can garner a better understanding of why a certain fund is being used. This allows us to give feedback to those managers. They may benefit from having a fiduciary inform them that we notice when they use their underperforming funds, and this feedback may lead to a change for the betterment of the participants. This system should be done only for active and blend managers. Index target date fund underlying strategies should be examined as well because some fund managers may be including indexes to get certain asset exposures. On occasion, these funds show significant tracking error.

Drawdown of Active vs. Passive

In terms of downside protection, it is important to examine the closer to retirement vintages and identify how these funds perform during times of heightened volatility. When looking at an average of -17% performance of those in a 2020 retirement vintage, the difference with active and passive management tells an interesting story. The largest index target dates by AUM lost on average -10.30% while active managers lost -8.54%, with some only showing a drawdown of -5.90%. This may speak to the potential benefit of active management and its role in security selection.

Security selection can be particularly important when the target date suites include categories like small cap and emerging markets that tend to be less efficient asset classes. Since active managers can underweight or overweight certain securities, they reduce the downside exposure of the fund by selecting those companies with better balance sheets and other fundamental qualities. With an index target date suite, the exposure to each asset class is comprised of securities found within that index fund. For example, some active managers were underweighted or had dropped their emerging markets exposure which benefitted them during the market drawdown in Q1 2020. On the other hand, those index target date managers who included emerging markets indexes saw a drawdown around -24%.

No target date is really “passive.” As target date funds continue to realize large inflows from retirement plans, employers and advisors must perform a holistic assessment of these funds and their managers. Underlying strategy evaluation and comparison is required. Downside protection must be considered.

Michael Garberich is an Investment Analyst at Leafhouse Financial. Todd Kading is President & Co-founder of Leafhouse.

©2020, Leafhouse Financial. Used with permission.