The number of 401(k) plans offering a Roth option has more than doubled over the past 10 years, according to the Plan Sponsor Council of America’s (PSCA) 60th Annual Survey of Profit Sharing and 401(k) Plans.

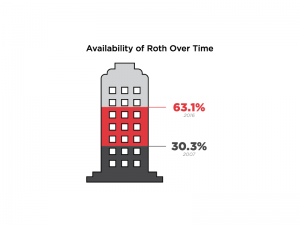

Nearly two-thirds of plan sponsors now provide a Roth 401(k) option, with more than 63% of plans offering the option in 2016, compared to 30.3% in 2007, according to the survey.

Other findings show that 7.2% of plans added a Roth option in 2016, with the largest increase at 11.2% for plans with more than 5,000 participants.

Meanwhile, almost one in five eligible employees (18.1%) made Roth contributions to a plan in 2016, which is up from being in the single-digit level just a few years ago. While it seems the overall contribution level is still somewhat low, the Roth 401(k) option wasn’t permitted until the 2001 Economic Growth and Tax Relief Reconciliation Act, and didn’t become effective until 2006.

Somewhat curiously, the highest percentage of Roth contributors came from participants in smaller plans. According to the findings, plans with 1-49 participants had an average of 29.2% of eligible employees making Roth contributions.

“In the 12 years since Roth became available as an option where you already offer a 401(k) or 403(b) with pre-tax contributions, Roth features have demonstrated their value,” observes Jack Towarnicky, PSCA Executive Director.

[caption id="attachment_80354" align="alignright" width="300"] Roth availability doubles in a decade.[/caption]

Roth availability doubles in a decade.[/caption]

Towarnicky suggests that in some situations, Roth contributions might be preferable to pre-tax contributions, such as for workers who:

- are just starting their careers and may currently be subject to a lower marginal income tax rate;

- seek tax diversification as a hedge against potentially higher future income tax rates in years to come;

- are employed in a state that doesn’t currently have an income tax;

- want to build a legacy accumulation of assets that will not be subject to minimum required distributions;

- are limited by the 2018 IRC Section 402(g) contribution maximum of $18,500 and/or the 414(v) catch-up contribution maximum of $6,000, and know that an equal amount of contributions on a Roth basis represents a significantly greater savings rate;

- are highly paid and are not eligible to contribute to an IRA on a Roth basis; or

- want to convert taxable monies to a Roth basis today, but are not currently eligible for a distribution that can be rolled over and converted into a Roth IRA (plans with Roth features can permit in-plan conversions at any time).

Additional information about purchasing PSCA’s 60th Annual Survey, which covers topics such as automatic enrollment, employee eligibility and investment advice, is available here.