Even as the potential opportunities and plan sponsors’ interest in health savings accounts expand, certain obstacles remain in advising clients about utilizing them, according to a recent survey of retirement plan advisors.

The cost of health care in retirement is a growing concern – and little wonder. Fidelity’s Retiree Health Care Cost Estimate recently said that a 65-year-old couple retiring in 2017 will need an estimated $275,000 to cover health care costs in retirement, up from an estimated $245,000 in 2015. At the same time, HSAs – long relegated to the realm of benefit advisors – have erupted on the radar screens of retirement plan advisors. It’s not just the triple-tax advantage of these accounts (pre-tax contributions, taxes deferred while in the account, and no taxes applied when withdrawn for designated purposes), though it certainly doesn’t hurt.

Two dynamics likely explain the surge; continued concern about health care costs, particularly on the part of employers, and the expanding availability of high-deductible health plans.

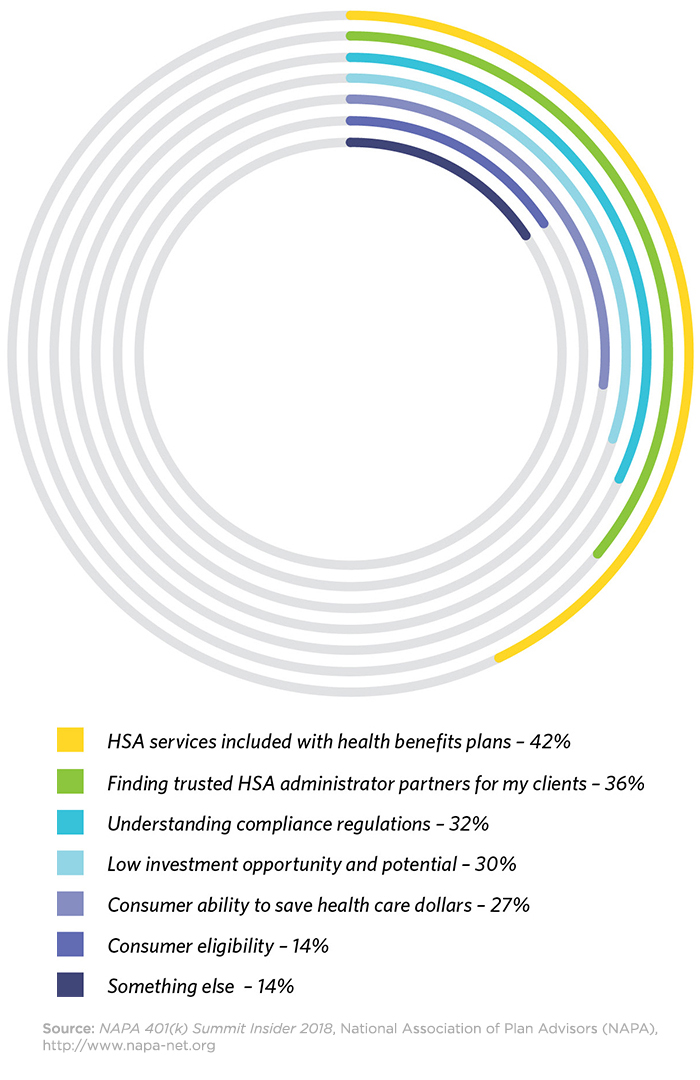

Indeed, according to a unique survey of more than 500 advisors who participated in the 2018 NAPA 401(k) SUMMIT Insider, the most commonly cited issue was that those HSA services are typically included with health plans. In fact, nearly half of the respondents cited that as one of the biggest challenges.

However, that wasn’t far ahead of the difficulties in finding trusted HSA administrator partners for their clients, cited by more than a third (36%) of advisor respondents. In fact, the challenges mentioned were quite varied, ranging from the 32% who cited issues with understanding compliance regulations to the 30% who noted “low investment opportunity and potential” and the 27% who expressed concern regarding consumers’ ability to save health care dollars.