The ERISA consultants at the Columbia Management Retirement Learning Center Resource Desk regularly receive calls from financial advisors on a broad array of technical topics related to IRAs and qualified retirement plans. A recent call with a financial advisor in Texas is a common inquiry involving IRS examinations of qualified retirement plans. The advisor asked:

Can you provide any insight into what the IRS looks for and the steps involved in examinations of qualified retirement plans?

Highlights of Discussion

• With respect to “what” the IRS looks for, while the IRS has the right to conduct a comprehensive examination of an employer’s qualified retirement plan, the top 10 most common areas of focus include:

1. Eligibility, participation and coverage

2. Vesting

3. Discrimination

4. Top-heavy requirements

5. Contribution and benefit limits

6. Funding and deductions

7. Distributions

8. Trust activities

9. Plan and trust documents

10. Returns and reports

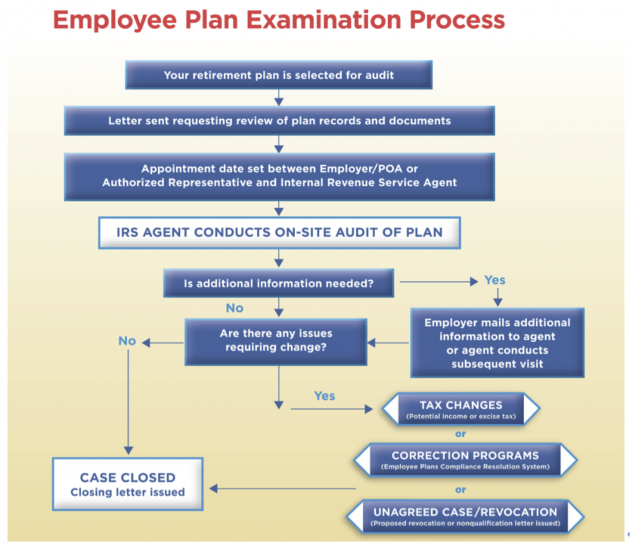

• The IRS has quite an extensive library of employee plan examination material online (at irs.gov), including this examination process chart and the top 10 most common areas of focus. (For a larger version in pdf format, click here.)

• As a best practice, you may want to use the following checklist with your plan sponsor clients regularly to help them determine whether their plans are IRS “audit proof.”

— Are eligible employees properly participating?

— Have service and vesting been properly credited?

— Do contributions, benefits, rights or features improperly favor highly compensated employees?

— Have minimum contributions and benefits, and accelerated vesting, been provided?

— Are contributions and benefits within applicable limits?

— Are contributions correct and timely made, and deductions within applicable limits?

— Are distributions correctly calculated, properly made and timely and accurately reported?

— Is the trust operated for the exclusive benefit of participants and in accordance with fiduciary standards?

— Does the form of the plan and trust meet applicable tax law?

— Were federal returns and reports timely and accurately filed?

Conclusion

No plan sponsor looks forward to receiving a letter from an IRS audit agent. Financial advisors can help reduce the angst plan sponsors feel by helping them audit proof their plans. Financial advisors who familiarize themselves with the IRS’ plan examination process and the top 10 items of review are better positioned to support their plan sponsor clients.![]()

The Columbia Management Retirement Learning Center Resource Desk is staffed by the Retirement Learning Center, LLC, a third-party industry consultant that is not affiliated with Columbia Management. For informational purposes only. Please consult a tax advisor or attorney for specific tax or legal needs. © 2013 Columbia Management Investment Advisers, LLC. Used with permission.