Ready, or not?

A phrase that’s heard with increasing frequency in both the defined contribution and HR worlds is “retirement readiness.” In the 2012 Defined Contribution Participant (DCP) Plan Sponsor survey of 2,800 comp and benefits directors, for example, 82% said they feel it is their “responsibility as a plan sponsor to make sure that their employees are tracking towards a comfortable retirement (i.e., retirement readiness).”

Furthermore, in a BRG/BlackRock study, 72% of plan sponsors said they agreed that it is their responsibility to “help employees get through retirement, not simply reach it.” Yet despite plan sponsors’ apparent sense of responsibility, there is a steady and increasing stream of studies concluding that employees are not prepared to retire.

So what can be done? And just as importantly, what role can advisors, who are a major force in the industry, play in the retirement readiness solution?

We all know a major hindrance to retirement readiness for millions of DC plan participants is leakage, in the form of cashing out their DC account balances when they change jobs or retire. Plenty of data are readily available on the magnitude of the problem at the DC level. But these industry-wide numbers on the amount lost due to leakage are so ponderously large, they actually tend to desensitize and discourage us from taking action.

The leakage problem will ultimately be solved one plan sponsor and one participant at a time. So let’s look at the impact on an individual participant’s retirement readiness.

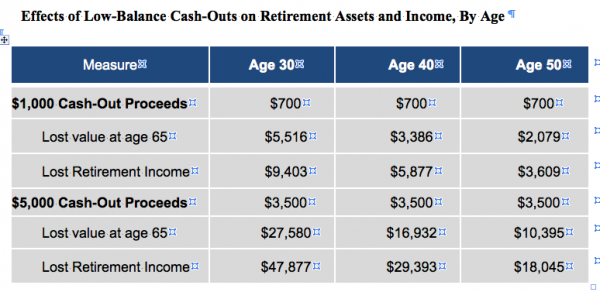

If a participant at age 30 cashes out $1,000 and nets $700 (which is probably spent quickly), he or she will forego a lump-sum value of $5,516 by age 65. That participant could have enjoyed $9,403 in total retirement income (“readiness”) from that single $1,000 by age 85 had it remained in the DC or IRA system.

If that participant cashes out $1,000 three times over the course of a career — let’s say at ages 30, 40 and 50 — the total loss of readiness is approximately $18,000. The same analysis for $5,000 cash-outs at ages 30, 40 and 50 shows the lost retirement readiness nears $100,000. (These are simply hypotheticals, but the projections are likely conservative, as EBRI estimates American workers will change jobs an average of 7.4 times in a 40-year career.)

Benefit Spend, or Spent?

These numbers are certainly troubling for the participant. But the equally troubling point is approximately 30% of these “lost dollars” are contributed to the participant’s DC account by the employer, whose sense of responsibility is to increase their participants’ retirement readiness directly and through market appreciation. Unfortunately, cashed-out benefit dollars leave the DC and IRA system and are rarely applied in other forms to retirement readiness. (It is, of course, recognized that DC plans are often offered to be competitive in labor markets, in addition to creating retirement readiness.)

Given the impact of cash-outs on their participants’ retirement readiness, and the fact that the problem persists, one wonders whether plan sponsors know the magnitude of the cash-out problem and/or if they are concerned about ex-employees who are cashing out.

Interestingly, in the 2013 version of the DCP Plan Sponsor survey, about half (53%) said they do not know what percentage of terminated or retired participants who took the money out of their DC plan cashed out their balances. Those who could give an answer cited an average 33% cash-out rate (actually pretty close to national norms). But furthermore, about four in 10 plan sponsors (39%) say they “are concerned about their employees’ cashing out.” This is fairly high, given that half of plan sponsors don’t even know the magnitude of their plan’s cash-out problem.

Game Changers

On a macro level, it makes financial sense for advisors to help solve the cash-out problem. That is, if the cash-out rate can be cut in half, $1.3 trillion will be retained in the DC/IRA system over a 10-year period, according to EBRI. That’s almost $400 billion that will potentially stay in the advisor channel.

On a micro level, there is also a substantial opportunity for an advisor (and/or recordkeeper) to help their clients in a meaningful way to making progress in retirement readiness. First, consider that, according to the 2012 DCP, plan sponsors have a low satisfaction rate with the recordkeepers’ education for departing participants regarding their withdrawal options and the financial ramifications of each option. The advisor — either alone or in collaboration with the recordkeeper — could step in and play a meaningful role in educating the participant and the plan sponsor. In fact, this is one of those rare cases where sheer information will change participant behavior.

Secondly, consider the fact that, according to the 2012 DCP, only half (52%) of plan sponsors are “very satisfied” with the (bundled) recordkeepers’ retirement readiness initiatives offered to their participants. The advisor can easily help the plan sponsor establish or outsource systems that assist employees in rolling over their balances to their next DC plan or to an IRA. (Most, but not all, systems and procedures available today actually make cashing out far easier for participants than rolling over the assets, our 2013 DCP Participant Study found.) Assistance in rolling over the balances is a highly valuable but low-cost (or no-cost) employee benefit. It is particularly valuable if it is “marketed” to participants at enrollment and throughout their time with the plan sponsor, since it is a benefit that virtually everyone will utilize someday.

These two steps alone will add substantial value to the advisor in the plan sponsor’s view by tangibly, inexpensively and effectively enhancing progress toward the key goal of retirement readiness, by keeping the sponsor’s benefit spend focused on its intended long-term purpose.

Warren Cormier is President and CEO of Boston Research Group and author of the DCP suite of satisfaction and loyalty studies. He also is co-founder of the Rand Behavioral Finance Forum, along with Dr. Shlomo Benartzi.