A recent World Economic Forum report, The Future of Jobs and Skills, included a list of the top 10 skills that will be valued most by 2020:

- Complex problem solving

- Critical thinking

- Creativity

- People management

- Coordinating with others

- Emotional intelligence

- Judgment and decision-making

- Service orientation

- Negotiation

- Cognitive flexibility

This list can be summarized in two words: behavioral governance. What will matter most by 2020 — no matter the industry sector or domain — will be a person’s ability to execute, infuse and amplify a prudent decision-making process.

In my last column, “To Prepare for the DOL Fiduciary Rules, You Need to Think BIG,” I introduced the concept of Behavioral Governance. Behavioral Governance is directed toward key decision-makers who have legal, financial, professional or moral liability for their governance process. This would include advisors, consultants, directors, trustees, officers, committee members and senior staff.

What does all this have to do with elite plan advisors? Everything.

By 2020, elite retirement advisors will be valued more for their behavioral governance than for their technical skills. And other points of differentiation — such as acknowledging fiduciary status — won’t mean a darn thing.

Continued advancements in the area of robo-advice and modeled portfolios, as well as the outsourcing of 3(38) services, will have the effect of diminishing the importance of a plan advisor’s technical expertise in constructing investment portfolios. So too, the DOL, armed with its new conflict-of-interest rules, is going to have the industry pole-vaulting over mouse turds.

The rules will maximize the number of advisors subject to fiduciary regulations; but, in so doing, minimize the actual value of a fiduciary standard.

Click here for a pdf of this column, and here to browse past columns by Don Trone.

Building upon the concepts introduced in that previous column, we’re going to add the concept of Neuro-governance, or Neuro-Fiduciary, to our framework.

Neuro-governance is the study of how physiology, cognitive psychological functioning and brain functioning influence the quality of a fiduciary’s decision-making process. (This definition of Neuro-Governance was developed by Prof. Sean Hannah and Dr. John Sumanth of the Wake Forest University School of Business, both of whom are associated with 3ethos.)

Stress, sleep, exercise, and even what one eats all have significant physiological and neurophysiological impacts on decision-making. Furthermore, a general understanding of neuroscience, such as executive control functioning, left and right hemispheric brain functioning, and the emotional centers of the brain and associated self-regulatory techniques, can improve an understanding of the factors that influence decision-making.

Elite plan advisors should be able to demonstrate a continuum among their Governance (prudent fiduciary process), Behavioral Governance (specific behaviors that amplify and help to predict the quality of a prudent process) and Neuro-Governance. When there is a continuum, we use the term, “Behavioral & Inspirational Governance” (BIG). (See Fig. 1.)

BIG provides the framework for answering such questions as:

- Does a fiduciary’s strong sense of authenticity and/or accountability (stewardship behaviors) influence a successful client engagement?

- How do levels of courage and commitment (leadership behaviors) influence fear, risk-taking and risk-aversion, which may alter the behavior of a fiduciary?

- How do the stewardship behaviors of attentiveness and adaptability influence the speed with which fiduciaries perceive changes in the marketplace and effectively react to them?

- How can an advisor’s leadership and stewardship behaviors influence the decision-making process of an investment committee?

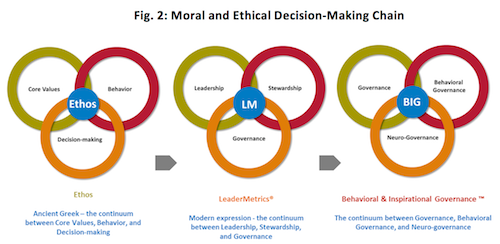

In turn, BIG helps anchor the evolutionary chain that we have been developing over the years to illustrate that the concepts of moral and ethical decision-making — of placing the best interests of others first — are as old as written and spoken language (see Fig. 2).

The DOL has created an industry crisis, and right now everyone is focused on overcoming the complexity of the new rules. However, our industry is resilient, and we’ll ride out this goat rodeo. When we do, we’re going to begin looking for a new professional standard of care, because fiduciary will merely define a de minimis standard.

By 2020, what will matter most will be the plan advisor’s ability to think BIG.

©2016, 3ethos. Used by permission.

Donald B. Trone, GFS® is one of the founders of 3ethos. This column appeared in the Winter 2017 issue of NAPA Net the Magazine. Opinions expressed are those of the author, and do not necessarily reflect the views of NAPA or its members.