Advisors are confronted with a host of new challenges – but what about the plan sponsors they support?

Well, according to a unique survey of more than 500 advisors who participated in the NAPA 401(k) SUMMIT Insider, plan sponsors – at least in the eyes of their advisors – are still, mostly, dealing with classic issues.

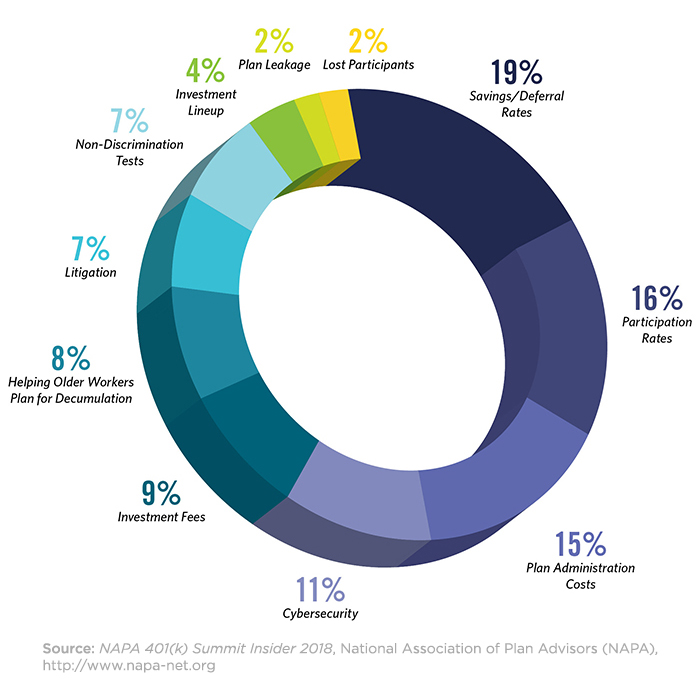

Asked to pick the three most significant concerns for their plan sponsor clients, savings/deferral rates, participation rates and plan administration costs dominated the choices, though cybersecurity, a relatively new concern, was a close fourth – though it came in higher (second place) according to advisors who primarily worked among plans above $100 million in assets – pushing aside participation rates.

In the “ad hoc” category, financial wellness popped up, as did “outcomes” generally. But perhaps the most surprising – at least due to its frequency – was general plan administration – or, as most termed it “administrative burdens.”

As one respondent explained, “As recordkeeping costs decline, so does the service level. Recordkeeping business models have become segregated, so the primary relationship manager is less involved with plan details since he/she is now managing significantly more plans.” Another cited the “increased administrative burden of administrating plans. Plan providers providing less and less service. HR managers are buried and it’s getting worse,” they said. “I find most sponsors have very rudimentary knowledge of their plan document provisions and even less about their responsibilities,” commented another.

“It varies from plan to plan, but I commonly hear complaining about the complexity of running a plan -- rules, regulations, disclosures, fees, fear of litigation, etc.,” explained another. “Most would refer to those things as the necessary evil for trying to help employees out.”

The survey found that among advisers “client retention” loomed largest for survey respondents, just ahead of fee compression, with a distant third being the fiduciary regulation.