8 months 1 week ago

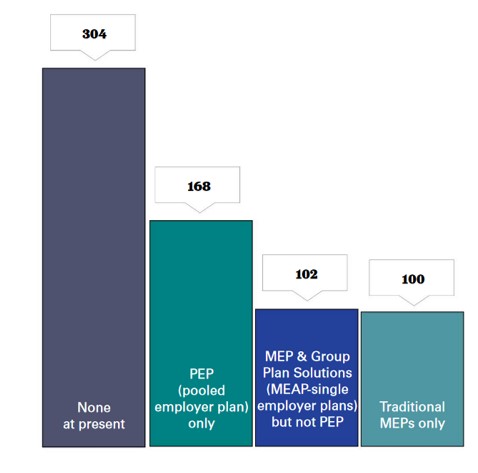

It appears that PEPs are outdistancing Group of Plans as a solution by almost a 2-1 margin. That gap will continue to expand, I believe, as more advisors get comfortable with pooled employer plans. We shall see.

Advertisement

One of the most-anticipated provisions in the SECURE Act was the advent of a new brand of multiple employer plan—now labeled a pooled employer plan, or PEP.

Created by the SECURE Act in 2019 and first approved for use in 2021, a PEP is a type of 401(k) plan that allows unrelated businesses to participate in one plan managed by a pooled plan provider (PPP).

Created by the SECURE Act in 2019 and first approved for use in 2021, a PEP is a type of 401(k) plan that allows unrelated businesses to participate in one plan managed by a pooled plan provider (PPP).

In fact, a recent survey found that more than half of smaller employers surveyed by LIMRA that are considering a DC plan are interested in learning more about PEPs—regardless of whether they have a retirement plan currently in place. At that time, LIMRA found that employers with 10–99 employees were significantly more interested in learning more about PEPs, especially the largest (small) employers (those with 50–99 employees).

That said, and as is often the case, those in favor of pooled employer plans seemed not only quite keen, but enthusiastic about the current state—and their prospects. And while there has certainly been a lot of PEP creation, the take-up—undoubtedly somewhat stymied by the onset of COVID-19—has likely been less than hoped overall.

That said—and perhaps indicative of the slow start—we asked Summit “Insiders”—more than 600 retirement plan advisor attendees at the 2023 NAPA 401(k) Summit—which of the following pooled plan solutions are you currently using, if any—and allowed for more than one response:

| None at present | 304 |

| PEP (pooled employer plan) only | 168 |

| MEP & Group Plan Solutions (MEAP-single employer plans) but not PEP | 102 |

| Traditional MEPs only | 100 |

Check out the rest of the 2023 NAPA Summit Insider at https://bit.ly/23Summitinsider1

Advertisement