The decision about when to claim Social Security retirement benefits is a topic that is well covered in the financial press since most American retirees either are currently receiving retirement benefits or can expect to do so. Research typically suggests that retirees, especially healthier retirees, are better off delaying claiming benefits given the current benefits formula.

There are a variety of factors that drive household decision making around claiming, which are covered quite extensively in some new research by Suzanne Shu and John Payne. For example, they find individuals who expect to live longer, have more financial patience, are less averse to losses, and have a lower sense of perceived ownership regarding benefits tend to claim at later ages, on average, consistent with expectations.

One especially notable finding that is contrary to expectations is that respondents who thought the Social Security trust was more solvent were more likely to say they would claim benefits earlier. This is the opposite of what you’d generally expect, whereby an individual who thought the program was less solvent would want to claim earlier (because they’d be concerned about the future likelihood of receiving benefits).

Thes findings have important implications given the media’s focus on the funded status of the Social Security system. While intuitively this focus could drive concerns that people would start claiming earlier, this research suggests the opposite. Regardless, additional research on how perceptions of the solvency of Social Security system is likely warranted.

What Drives Claiming Decisions?

There are decades of research exploring the factors related to when people claim, or are expected to claim, Social Security retirement benefits. The body of literature is at least partially due to the economic implications associated with the decision, where the present value of benefits can easily exceed $1 million for a household and suboptimal decisions around claiming could cost $100,000 or more.

Research has generally suggested retirees who have the means to do so should consider delaying, given the fact benefits are tax advantaged, explicitly linked to inflation, and offer spousal protection. While most Americans claim before their full retirement age (~67), claiming ages have been rising over time, which is likely at least partially related to the increase in workforce participation among older Americans.

In some recent research for NBER, Suzanne Shu and John Payne explore the individual differences in beliefs and values that influence Social Security claiming intentions. As expected from economic theory, individual differences in life expectations and degree of patience for later larger payouts relate to claiming intentions. In addition, they find that individual differences in psychological ownership of one’s Social Security benefits and individual differences in degree of loss aversion are both significant predictors of Social Security claiming intentions.

Further, they find that an “enriched” information display manipulation (nudge) that emphasizes longer-term consequences of late claiming leads to earlier, not later, claiming intentions, and that the size of this effect is related to individual differences in the degree of loss aversion.

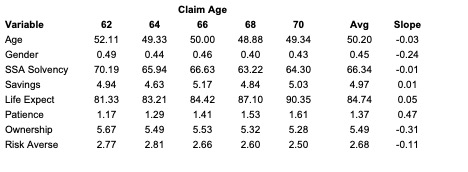

They include five potential claiming ages (62, 64, 66, 68, and 70) in a series of surveys, where the resulting data is available online:

https://osf.io/ut84j?view_only=7c5481c9b9b64a8c841d3a872e97f9e0.

The exhibit below includes the average values for different variables, by claiming age, across all four surveys (N=4,191), which is similar to Table 4 in the piece.

Source: Dataset for “Social Security Claiming Intentions: Psychological Ownership, Loss Aversion, and Information Displays” by Suzanne Shu and John Payne. Created July 17. 2023. Available here: https://osf.io/ut84j?view_only=7c5481c9b9b64a8c841d3a872e97f9e0.

The averages provide context about how things change by claiming age, as do the slopes. A positive slope would mean as that variable increases claiming ages increase. For example, as someone expects to live longer (have a longer life expectancy) claiming ages tend to increase, consistent with expectations and an effect that is obvious just looking at the average values.

One relation that’s especially surprising is how perceptions around the solvency of Social Security vary by claiming age. For reference, the question asks for the respondents estimated probability that the Social Security Administration will exist to pay future benefits, where the scale is 0 to 100. One would expect individuals who claim at earlier ages would have lower solvency expectations since that would imply a higher probability of not receiving the higher delayed benefit, but the opposite is actually the case.

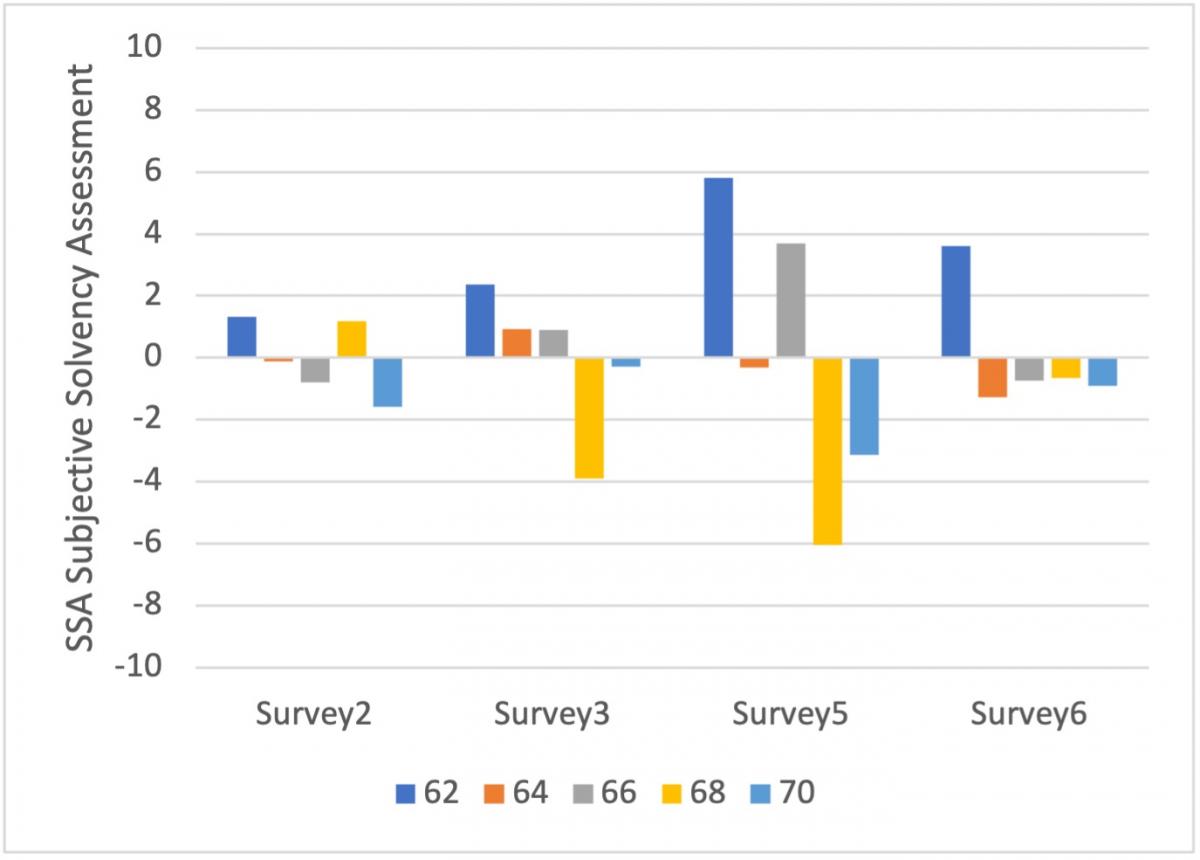

The previous table included the averages across the four surveys conducted. Since there are notable differences in values across the four individual surveys, the next exhibit includes the difference in the subjective Social Security solvency level for each of the four surveys by claiming age (averaged by that survey), to provide some context around the robustness for the solvency relation across the surveys.

Source: Dataset for “Social Security Claiming Intentions: Psychological Ownership, Loss Aversion, and Information Displays” by Suzanne Shu and John Payne. Created July 17. 2023. Available here: https://osf.io/ut84j?view_only=7c5481c9b9b64a8c841d3a872e97f9e0.

For each of four the surveys, those who forecasted the highest solvency level claimed at the earliest possible age (62). Again, this is counterintuitive, since one would expect respondents would be more willing to claim later if the system was perceived to be more solvent, but the reverse was the case.

The relations remained after controlling for other variables in a series of regressions, which are included in the research paper, suggesting the effect is both economically and statistically significant.

What Next?

The decision around claiming Social Security retirement benefits is very personal, but is one of the most important decisions household make with respect to retirement. There are a number of variables that have somewhat intuitive relations to when people claim, or expect to claim, Social Security retirement benefits, such as life expectancy, risk aversion, a sense of ownership, etc.

One variable that has a counterintuitive relation with Social Security claiming is expectations around solvency, where respondents who thought the system was more solvent, claimed earlier on average. This is the opposite of what was expected. The good news with this relation is that it at least suggests that media coverage on the underfunded status of the Social Security trust fund is unlikely to (materially) affect claiming decisions; however, more research on the degree to which solvency could affect claiming decisions is definitely warranted.

David Blanchett is Head of Retirement Research for PGIM DC Solutions. PGIM is the global investment management business of Prudential Financial, Inc. David is also currently an Adjunct Professor of Wealth Management at The American College of Financial Services and Research Fellow for the Alliance for Lifetime Income.