To view a PDF version of this article, click here.

Would people save more for retirement if they knew their current rate of saving was inadequate? Intuition tells us many people would. And now, so does the data.

Surveys have long shown that people who say they have a good handle on their retirement readiness are also more likely to say they engage in “good” saving behaviors. Today we have numbers to validate their story. A representative sampling of defined contribution plans administered by Transamerica finds that participants who have viewed a personalized retirement outlook — an assessment of their retirement readiness that can be calculated quickly, online — are saving on average 6.44% of their salaries for retirement. By contrast, those who have not viewed a retirement outlook are saving just 3.76%, a difference of 268 basis points.[1].

How significant is that? If we compound the savings over a 40-year career, assume average annual investment returns of 6%, and use a starting salary of $40,000 that increases 3% annually, the person saving more of their salary will end up with $259,000 in additional cash at retirement age. Plug in a $75,000 starting salary, and the difference becomes approximately $486,000.

Why do people who’ve viewed their retirement outlook save so much more than those who haven’t? Perhaps it is for the same reason that people with maps are more likely to reach their destination than people who only guess where they’re going. Information is empowering. It drives and enables better decision-making. An easy-to-grasp retirement outlook lets people know where they stand, even if the outlook is gloomy. It helps them take stock of their situation, and presents them with an opportunity to chart a new course.

Here’s some proof. In a survey of plan participants last year, 55% of those who received a negative retirement outlook said it motivated them to develop a plan to enhance their retirement readiness. A third of the respondents actually increased their deferral rates, and 19% changed the way their plan assets were allocated. Another 17% consulted with a plan representative to explore options for improving their retirement outlook.[2]

The retirement outlooks that drove these behaviors were generated in some cases at the request of the individual participant and in others by the plan provider on the participant’s behalf. Either way, each outlook became part of the participant’s record and was subsequently conveyed to them multiple times in many different but always personalized ways — on their account statements, on the home page of their retirement plan website when they logged onto it, and via any mobile applications they used to access account information.

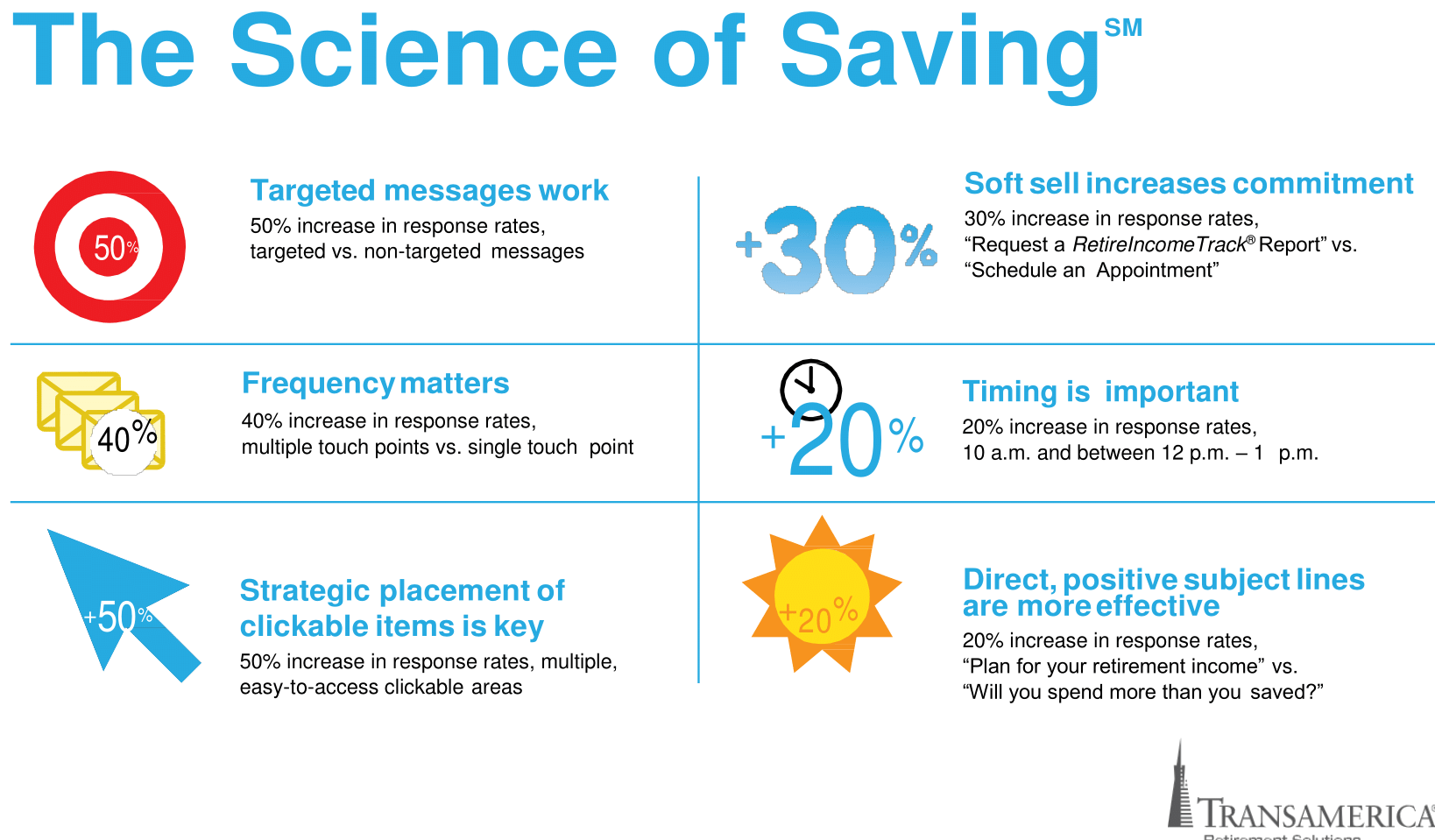

The Power of Engagement

Multiple points of contact like this are important because they promote the participant’s engagement with their retirement plan, and engaged participants are more likely to achieve retirement success. Research shows, for example, that doing something as simple as sharing their email address with their plan provider is an indicator that a plan participant will save more for retirement. In one recent sample, participants who provided email addresses were deferring on average 8.41% of their income into their retirement plans, versus 5.61% for those who didn’t supply an email address. That’s a difference of 280 basis points, and using the same parameters from our earlier examples — 3% annual salary increases and a 6% rate of return over a 40-year career — would result in nearly $271,000 in extra savings for someone who starts with a $40,000 annual salary It would provide an additional $507,000 for someone starting their career earning $75,000 a year.

That average disparity, by the way, only tells part of the story. In some demographic groups, differences in saving rates were astonishingly higher. Among plan participants in the higher education market, those who shared email addresses were deferring 400 basis points more of their salary, on average, than their peers who hadn’t shared an address. Among participants 70 and older in the corporate sector, the difference was 509 basis points. In fact, in three of the four sectors examined — higher education, corporate and manufacturing — the older participants were the more likely they were to be saving more if they had also shared their email address.[3] The only sector where that wasn’t the case was in retailing.

These surprising findings reinforce the idea that email is the best way to engage retirement plan participants. Using email, plan providers are able to connect with participants and prompt them to take action in ways that paper communications simply don’t allow, in part because email can be embedded with instantly actionable links while paper correspondence cannot. Providers also can more easily track how participants respond to email — how often they actually open their mail and how often they click through to take action — and this, too, can help providers refine their message to drive better saving and investing behaviors among plan participants.

Importantly, engaged participants don’t just tend to be better savers, they also tend to be more goal-oriented, and that also makes a difference in retirement readiness. Our research has shown that participants with retirement income goals defer a higher percentage of their earnings into their retirement savings plans, have higher account balances, and are more likely to be on track to reach their retirement goals. They also are more likely to read educational materials relating to retirement planning, and to use retirement planning tools, including retirement readiness calculators.[4]

Form Counts

How participants receive information about their retirement outlook is just as important as how often. Effective retirement readiness scoring systems deliver complex information in simple and intuitive form. The system used for the surveyed plan participants illustrates their overall retirement readiness with a simple weather-themed graphic: a rain cloud for participants at greatest risk, a bright sun for those in the best shape, and “cloudy” and “partly sunny” graphics for those in between. The goal of this sort of simplicity is to inform and educate without intimidating or overwhelming participants. To promote action, these simple messages are accompanied by a list of measures participants can take, sometimes with a few clicks on their computer, to immediately begin improving their retirement readiness.

Although many factors play into a retirement plan’s success, none is more important than ensuring that participants save at adequate levels. Providing participants with simple-to-understand retirement readiness scores on a regular basis, and utilizing email campaigns that make it easy for participants to refine their saving and investing behaviors, can go a long way toward helping them map a route to retirement success.

Footnotes

[1] As of March 1, 2015.

[2] Q1 2014 Transamerica Retirement Solutions’ Participant Survey of 2,073 participants selected at random.

[3] Participants in defined contribution retirement plans for which Transamerica serves as record keeper, as of June 30, 2014.

[4] Q1 2014 Transamerica Retirement Solutions’ Participant Survey of 2,073 participants selected at random.

Patricia Advaney is Senior Vice president, Customer Experience, for Transamerica.

This article originally appeared in the June 2015 Special Outcomes Issue of NAPA Net the Magazine.