To view a PDF version of this article, click HERE.

Baseball season is upon us, and with it comes a flurry of statistics. Not only do we get the daily box score of runs, hits and errors, but we now get to enjoy things like on base percentage for hitters and earned run average for pitchers.

And it doesn’t stop there. An entire new community of statistics called "Sabermetrics" has arisen to further differentiate one team or one player from another. Sabermetrics was made popular by the movie Moneyball — which is a movie that in my opinion is much more about innovation than it is about baseball statistics.

This obsession with statistics or metrics in baseball is best exemplified when you watch ESPN and hear something like the following: "That is the first time since 1987 that someone has hit to right field four times in a row when facing a left-handed pitcher in the month of May when the temperate was above 83 degrees" … which feels both truly obscure and relatively meaningless (only because it is).

The Outcome of Outcomes

As someone who has been in this industry for more than 30 years, it is a pleasure to see the incredible attention being placed on retirement outcomes. This focus should be somewhat expected given the "exclusive benefit" rule from ERISA, which states:

"A qualified retirement plan is required to be maintained for the exclusive best interests of the participants and beneficiaries and payment of reasonable administrative expenses."

So it is only natural that improving retirement outcomes would eventually become an area of intense focus for our industry. In addition, there is more and more research informing plan sponsors that improving retirement outcomes is not just a "feel good" thing — it is also good business. In essence, helping people retire well or even early will lead to lower labor costs, lower benefit costs, lower absenteeism costs and improved employee morale and engagement — all of which are good for a company’s bottom line.

Thus, if you are a service provider and there is a "thing" that is "good" for both of your customers (your plan sponsor client and their participants), then it makes complete sense that you should care about that "thing." This helps explain the recent emphasis on retirement outcomes from service providers.

There is, however, a recent phenomenon that in my opinion has also accelerated this focus on retirement outcomes, and that is the other part of the exclusive purpose rule shown above: the focus on what are "reasonable" service provider fees.

Based on public information, it appears that more $320 million in lawsuits have been settled or awarded related to fee litigation of retirement plan service providers. In almost every one of these situations, there has been a reference to the impact that fees have on retirement outcomes. So let’s run through a relatively simple example to see just how much you can improve retirement outcomes by cutting fees.

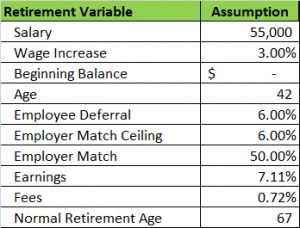

First, Table 1 shows some very simple assumptions that are relatively typical for our industry.

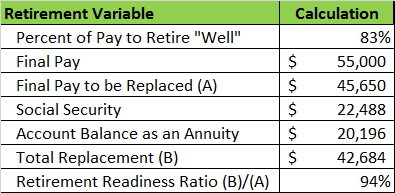

Based on these assumptions, this individual will have a retirement readiness ratio of about 94% in today’s dollars (today’s dollars can be easier for participants to understand). This is illustrated in Table 2.

Not bad, but not quite 100%.

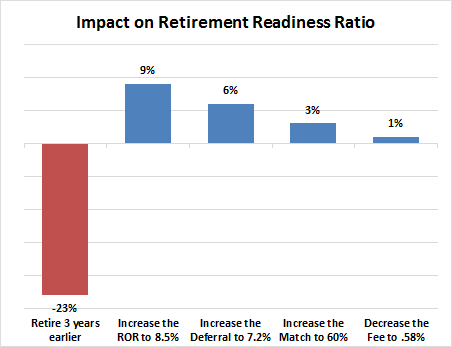

Now, let’s conduct a sensitivity analysis where we change five different variables by 20%:

- Retiring 3 years early at age 64

- Increasing the 7.11% rate of return by 20%

- Increasing the 6.00% employee deferral by 20%

- Increasing the employer match of 50% by 20%

- Decreasing the 72 basis point fee by 20%

The question is: which of the above variables do you think will have the greatest impact on the retirement readiness ratio for this individual? At FBi, we have analyzed this problem and publicly presented our findings since our first speech in 2009. We always ask people which item do they think will have the biggest impact and almost nobody picks the right answer, which is shown below in Fig. 1.

So, there is no doubt that fees have to be reasonable. That is the law and that is what participants deserve. But as Fig. 1 shows, to examine fees without looking at value could really hurt participants in a most severe manner. For example, imagine a plan where the fees are really low but participants do any or all of the below:

- They retire too early because they are not informed.

- They save too little because they are uninspired.

- They invest poorly because they are not properly guided.

A combination of these items would far outweigh the positive impact of a lower fee. To state the case more clearly using a "Captain Obvious" moment: "How can lower fees help someone not participating in the plan?"

This is probably why the DOL notes the following in their "Handbook on 401(k) Plan Fees": "Don’t consider fees in a vacuum. They are only one part of the bigger picture including investment risk and returns and the extent and quality of services provided."

So kudos to our industry for the intense focus on retirement outcomes. But let’s make sure we understand which retirement variables truly drive such success and which others are of minor importance. To quote the great management guru Peter Drucker: "What gets measured, gets managed." Let’s just make sure we are measuring the whole dog and not just the tail, because this is what participants deserve from our industry.

And that is the legal and social responsibility we assume as service providers on the behalf of millions of participants.

Tom Kmak is the CEO of Fiduciary Benchmarks.

This article originally appeared in the June 2015 Special Outcomes Issue of NAPA Net the Magazine.