As plan sponsors eye solutions for retirement readiness, personalization through the potential use of managed accounts and other personalized financial wellness offerings has become a major area of focus, according to a new white paper by Cerulli Associates.

In The Benefits of Personalization in Defined Contribution Plans sponsored by Edelman Financial Engines, the paper reveals that more than a third (36%) of 401(k) plan sponsors cite improving retirement readiness as the top priority for their 401(k) plan.

In The Benefits of Personalization in Defined Contribution Plans sponsored by Edelman Financial Engines, the paper reveals that more than a third (36%) of 401(k) plan sponsors cite improving retirement readiness as the top priority for their 401(k) plan.

A challenge, however, for key decision makers at some of the nation’s largest corporate defined contribution (DC) plans is selecting the right personalized financial services for their participant base—particularly as the needs of plan participants shift and expand. Among other things, these plans typically have diverse participant populations with varying levels of wealth, financial challenges, objectives and preferences, the paper notes.

And with an array of personalized financial services and providers from which to select, plan sponsors must determine which type of personalized solution and which solution providers are the best fit for their participant base. What’s more, accommodating the needs of heterogenous plan participants requires programs and features that can fill in gaps left by target-date funds or other less personalized offerings, the paper emphasizes.

“As fiduciaries, we want to make sure the [personalized solution] delivers value and makes sense for at least some portion of our participant base,” the head of global benefits for an asset management firm who participated in the research was quoted as saying.

Managed Account Solutions and Drawbacks

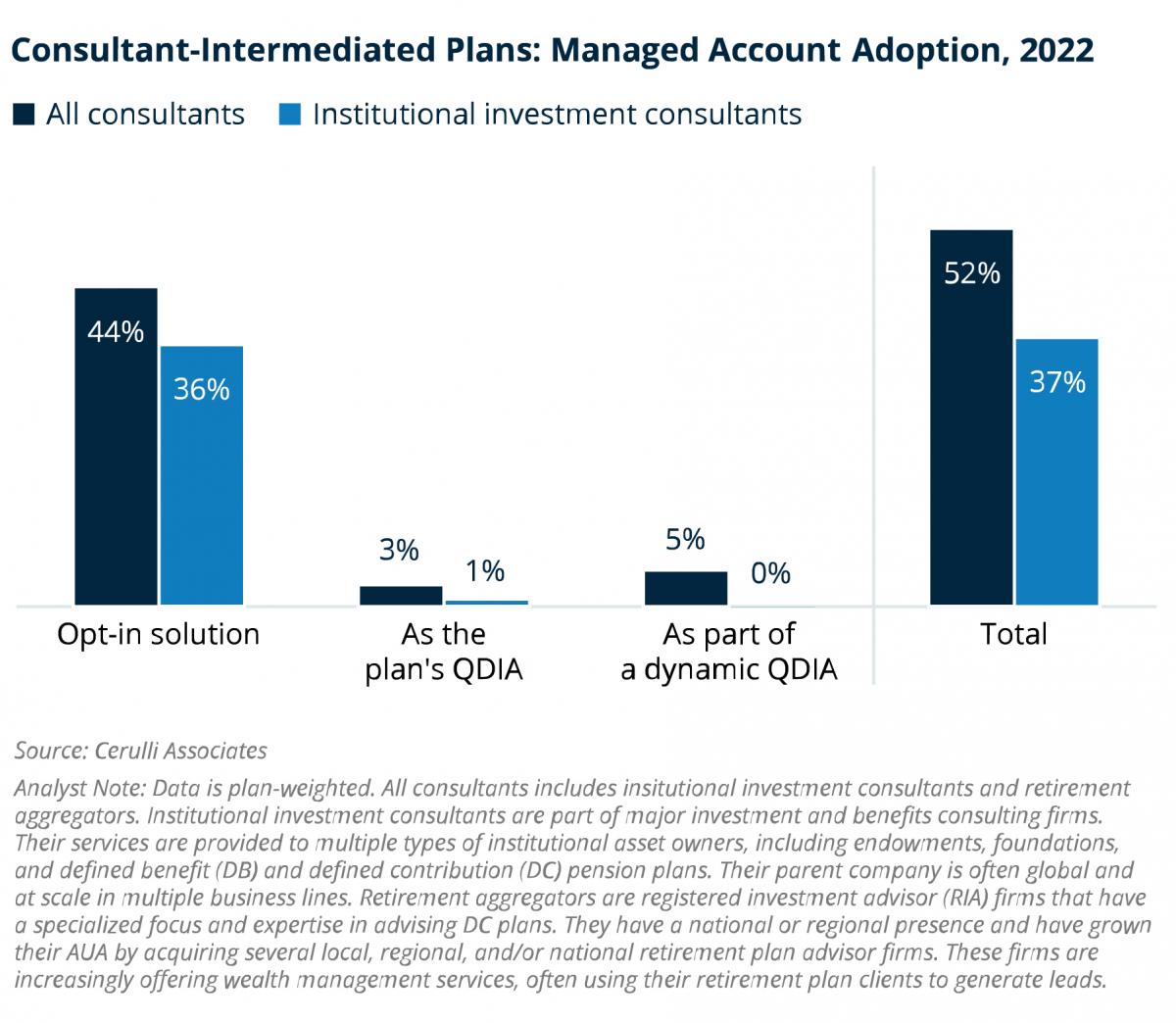

To that end, more than half (52%) of consultant-intermediated DC plans look to managed account programs to provide participants with greater access to personalized investment advice. Cerulli notes, however, that some plan sponsors seemingly “underestimate the value” managed account programs can deliver to participants. In conversations with Cerulli, several plan sponsors revealed that they compare the investment performance of managed accounts to associated target-date fund vintages.

What’s more, many plan sponsors that do not offer managed accounts either do not subscribe to the concept from a cost/benefit standpoint, offer participants financial advice or guidance in another capacity or are considering offering one, the paper further explains. “Given the looming risk of class-action litigation in the ERISA-covered DC space, fees are understandably important to large plan sponsors and their consultant partners as they consider any investment or plan-level service,” the paper states. In addition, pricing relative to target-date funds often deters them from offering the managed account as the QDIA. At the same time, however, recent class-action litigation accusing plan sponsors of focusing exclusively on fees in their selection process signals that defaulting to the lowest cost option will not necessarily insulate them from litigation.

“When evaluating whether or not to offer a managed account program, plan sponsors should look beyond the investment returns to uncover the full value that these programs deliver to participants,” notes Shawn O’Brien, director of the retirement research practice at Cerulli. “Financial planning and wellness features, and the ability to speak with an advisor, may have a meaningful impact on participants’ financial outcomes. Nevertheless, plan sponsors may need to employ different performance evaluation approaches to quantify their impact,” adds O’Brien.

As to which participants might benefit the most, Cerulli notes that, while affluent participants may appreciate the benefits of DC managed account programs, many of these individuals tend to have a wealth management relationship with an advisor outside of the plan. Consequently, the paper suggests that mass-market and middle-market investors (investors with less than $500,000 in household investable assets) and certain mass-affluent investors (with $500,000 to $2 million in household investable assets) approaching retirement are most likely to benefit from a DC managed account program, as opposed to seeking professional advice outside of the plan.

In fact, plan sponsors regularly highlight the importance of giving their participants access to a financial professional who can help them sort through key financial dilemmas in a holistic, nuanced manner.

As one plan sponsor explains, “In times of stress, they [participant] call one of the advisors from our managed account program, who are very well trained, and they [advisors] help people from doing something crazy. You have to think about what that is worth to somebody. It’s not about whether you call all the time, it’s that one call that keeps you invested and saves you a couple hundred thousand dollars.”

Cerulli’s research further shows that 401(k) participants value the ability to speak with an advisor when it comes to making key financial decisions. More than half (52%) of 401(k) participants would prefer to speak to a financial professional over conducting the research themselves (33%) or leveraging the advice of other connections, such as friends and family members (15%), when making a change to their finances.

Considerations

In considering personalized solutions, the paper suggests that plan sponsors and their consultants should assess the broader implications of specific program features. In addition to evaluating more-technical due diligence items (i.e., investment methodologies), sponsors should consider the potential benefits of providing access to human advisors, limiting potential conflicts of interest, and providing participants with a broader range of personalized advice via value-add programs, such as financial wellness and planning.

In fact, perceived conflicts of interest between managed account providers and participants are a major factor when evaluating managed account programs, the paper further emphasizes. It notes, for instance, that “recordkeepers offering a proprietary managed account program will, at times, offer plan sponsors steep discounts on recordkeeping administration fees in an attempt to win managed account program placements. However, some plan sponsors are rightfully skeptical of their recordkeepers’ motives for offering such steep discounts on either their recordkeeping administration or managed accounts,” the paper explains. As such, plan sponsors should be cognizant of these conflicts and actively address them with managed account providers when they do arise, the paper further advises.

The findings in the white paper are based on 19 interviews with key decision makers at large (greater than $250 million in assets) DC plans, including both plans that use and do not use managed accounts. The interviews did not reveal Edelman as the sponsor of the research. The paper also draws from Cerulli’s 401(k) Plan Sponsor Survey, 401(k) Participant Survey and DC Consultant Survey.

Access to the full whitepaper is available here.