One of the provisions of SECURE 2.0 that goes into effect Jan 1, 2024, is the requirement that all catch-up contributions be Roth contributions for participants earning more than $145,000 or more per year. Because of the complexity of administering this, many in the industry are pushing for a delay in the implementation date.

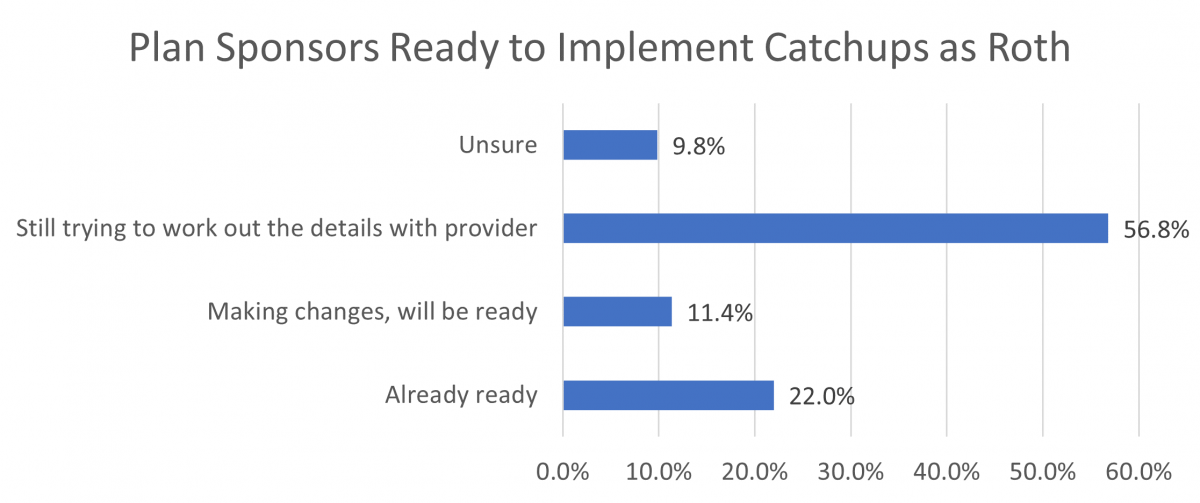

Members of NAPA’s sister organization, the Plan Sponsor Council of America, were recently surveyed about their readiness to implement this provision—and only a third are or will be prepared to implement it as of Jan 1, 2024. Most plan sponsors (nearly 60%) are waiting for guidance from their providers on how it should be implemented.

As the primary concern is the ability of the payroll provider and recordkeeper to have the technology in place to implement in time, several plan sponsors are working on a manual process as a backup plan in case the automatic processes are not in place in time so that they can continue providing catch-up contributions to participants. Select comments are included below.

Ready (or will be)

- The only change we need to make is to add an indicator on our payroll feed to the recordkeeper to designate those not eligible for pre-tax catch-up.

- We are moving to a new recordkeeper effective October 1, 2023, and will be ready. We already had the Roth option in our 401(k)-plan lineup.

- Already have Roth implemented.

- We already have the Roth selection -- waiting on Payroll provider for implementation instructions.

- We have a Roth option; therefore, believe we will be all set to implement.

Waiting on Provider Guidance

- ADP hasn't communicated a solution yet.

- Also, waiting on guidance so we know what the full options are. i.e., can we just make all catch-up Roth contributions or at least offer it to all?

- Are you kidding me? I want to know who has a payroll provider who has this programmed yet. My provider won't even work on it until they get answers to their questions in the form of guidance. We expect this to be a down to the wire kind of thing unless ARA and others are successful in getting an extension.

- I hope it's delayed. ADP has no solutions yet.

- I would prefer a delay since our payroll provider seems to be struggling with it.

- It appears that this is yet another complicated provision in which we will not be able to apply a systemic solution and will have to manage manually.

- Not likely ready 1/1/24

- Payroll reporting and internal controls are in place.

- Seems like providers, both payroll and recordkeepers are strongly pushing for a 2-year delay.

- Since we already offer Roth contributions in the Plan, we just need our payroll provider to implement the catch up rules, however, they have not been forthcoming with their Plan or timetable and that makes me unsure. We do not want to discontinue catchups!

- Still waiting on provider to give us details on how they will be reporting to us.

- The recordkeeper and the payroll providers are taking their time. I work for partners who get a K-1 and don't pay FICA. How are we supposed to determine if they will be affected by this provision. We clearly need more guidance.

- This provision needs a postponement. This is too quick.

- This requires changes to set up that most EMS and plan administrators are not ready to implement.

- Very unlikely we will be fully ready based on where our payroll provider is currently with their readiness.

- Very unsure about payroll provider readiness, but our recordkeeper is working on a workaround just in case. If we have to go with the workaround it is expected to be very manual, and with anything manual there is always a concern about mistakes. I am still praying that legislation is passed to push the deadline back.

- We already allow for Roth, but we are trying to implement the catch-up piece and compensation. It's challenging to try to automate this process.

- We already offer Roth so hopefully this won't be a huge change for us. Our provider hasn't given us details on how this will work so we're waiting to hear from them. It will affect most of our employees who contribute with catch up contributions so we're working with our brokers on the education/notification piece to make sure they're aware and understand the new rule.

- We already offer the Roth. Need to decide if we are making all catchup contributions Roth, or how to work with our HRCM and recordkeeper on how to identify staff who made over $145k in the previous year.

- We are considering dropping our Age 50 Catch-up provision due to the time it will take to make system changes and implement Section 603 of SECURE Act 2.0

- We are currently reaching out to our recordkeeper and payroll provider for updates and are planning to implement ourselves if providers are not ready. We are still hoping congress will provide some relief but are not counting on it.

- We are going to have to be ready. ; )

- We are waiting for ADP Vantage and T. Rowe Price to tell us how they will program for it.

- We do not have a great solution worked out with recordkeeper - current solution shifted responsibility to payroll provider.

- We have a Roth in our plan but we transmit to our recordkeeper automatically from our payroll system. Neither company has provided info on how this will work going forward.

- We have Roth contributions already set up, but our Payroll provider hasn't provided any guidance on how to make this work.

- We intend to comply but may need to utilize interim short term processes to make it work before we can have a fully automated process delivered by our payroll provider and recordkeeper.

- We need more time—need to set up in our plan, work with payroll, educate employes.

- We will be ready only if our vendors provide solutions for this. I think most of them are waiting for the government to provide more information.

- Will affect very few participants. A lot of work for little results

- With all the technical issues TPAs, Payroll companies and employers are up against a delay in provision would be prudent.

Unsure

- The IRS needs to provide more details for us to be able to find a fix and test before we have to notify participants that the change is coming.

- This provision seems like it has administrative nightmare written all over it! I am unclear as to the benefit to anyone of this provision.

- Understanding that Fidelity is working on it, but our payroll company has not said anything about it.

- Waiting on our HRIS vendor to get this set up.