Notwithstanding various market challenges, and buyers and sellers coming to the table with differing motivations and expectations, registered investment advisor (RIA) M&A activity has continued at an epic pace and is not expected to slow down.

From January 2020 to March 2023, RIA M&A deals increased 237%, with 492 transactions reported, compared to 146 for the previous study period of 2017-2019, according to Fidelity Investments’ 2023 M&A Valuation & Deal Structure Survey.

From January 2020 to March 2023, RIA M&A deals increased 237%, with 492 transactions reported, compared to 146 for the previous study period of 2017-2019, according to Fidelity Investments’ 2023 M&A Valuation & Deal Structure Survey.

The survey, which examines trends and buyer perceptions related to RIA M&A transactions, also found that buyers reported larger deals versus the previous study period, with the median AUM of acquired firms increasing from $250 million to $400 million.

Deals have also been closing at a swifter pace with an average deal completion time of roughly seven months for the last three years, down from nine months in the 2017-2019 period. However, more than one in three buyers agreed that recent market volatility has affected deal completion time.

When asked about deal sourcing, most firms reported that they were either sourced by in-house experts or investment bankers. Nearly half (45%) of firms disclosed that deals were financed using in-house capital, with a quarter reporting the use of private equity partners or draw loans.

The study, which was last conducted in 2019, surveyed serial acquirers involved in nearly 500 deals over the last three years and accounted for virtually 75% of all RIA transactions tracked by Fidelity during that time.

“Despite market headwinds, the wealth management industry continues to be a vibrant space for M&A, with the environment rewarding high-quality firms with strong multiples,” notes Laura Delaney, Fidelity’s vice president of practice management & consulting. “Although activity has increased substantially vs. the previous study period, it’s important for RIA business owners to align on valuation drivers and understand the dynamics involved in the motivations and expectations of buyers and sellers.”

Misalignment on Deal Valuation

In fact, buyers reported walking away from roughly half (52%) of evaluated deals. Key drivers leading to this were the misalignment of:

- valuation expectations (87%);

- culture (73%); and

- the firm’s vision (50%).

Of the deals which fell through specifically due to sellers’ unrealistic valuation expectations, unrealistic comparison multiples (83%), the lack of understanding of valuation drivers (77%) and being too close to the business to see weaknesses (47%) were the major factors leading sellers to overvalue their business.

Interestingly, Fidelity found that nearly half of sellers (49%) utilized a third-party for firm valuation. From a buyer’s point of view, 33% of deals had higher valuations for firms who used a third-party versus comparable firms who self-calculated.

“The nature of deals will continue to evolve,” Delaney further emphasizes. “We’re seeing strategic acquirers become increasingly efficient which is reflected in reported deal completion time, however, opportunity can be left on the table due to misalignment of dealmaking fundamentals. There’s an element of emotion behind every transaction.”

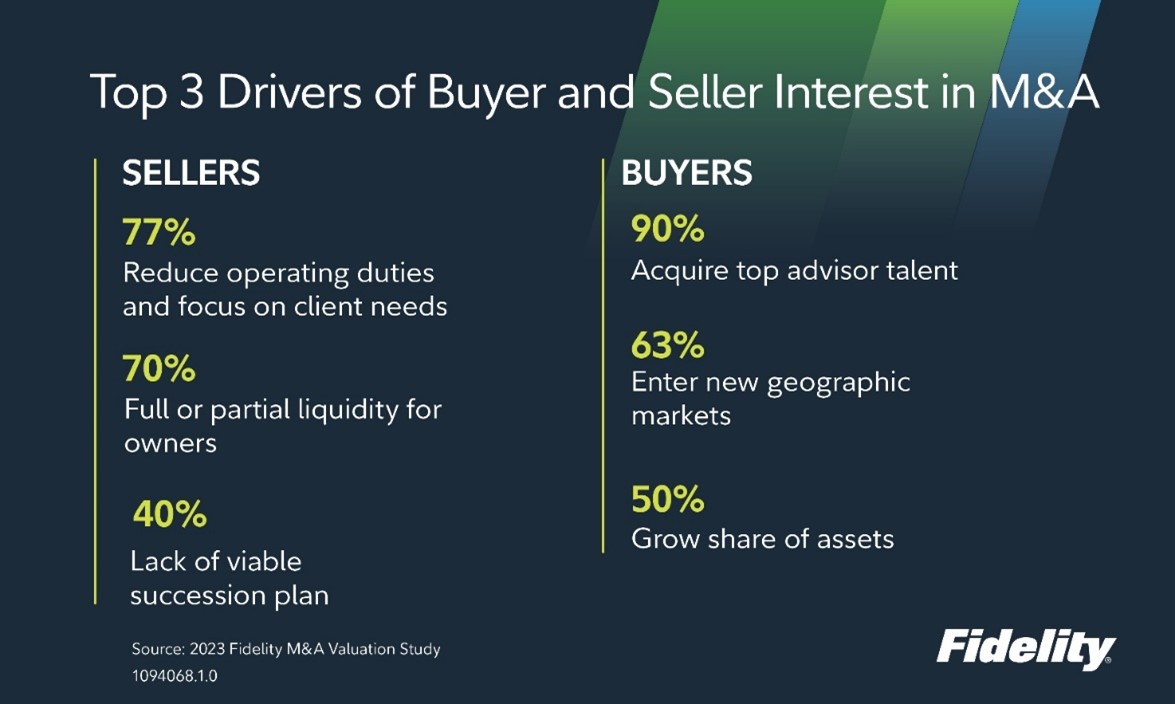

Differing Motivations

The research revealed that when it comes to making a deal, buyers and sellers come to the table with differing motivations and expectations.

If buyers and sellers can better understand each other’s key motivations, each can ensure they are effectively communicating the value their firm brings to the table, Fidelity notes.

When asked about expected deal activity in the next five years, three out of five firms plan to do more deals. According to the findings, this stems from: 1) a fragmented wealth management industry, 2) advisors continuing to age out of the business, and 3) firms continually seeking access to talent and scale, among other things.

Deal Structure

The study also examined changes in deal structure and found that buyers have evaluated nearly four times as many deals since January 2020, with median deal size increasing from $250 million in the 2019 study period to $400 million in the 2023 period, as noted previously.

Revenue multiples have also climbed from 2.25x to 3.25x. Median EBITDA (earnings before interest, tax, depreciation and amortization) multiples also increased from 7x to 9x, with sellers’ expected EBITDA multiples rising from 9x to 11x in the past three years, Fidelity notes.

The reported drivers of this increase include high organic growth, young and aggressive next-gen leaders, and a key geographical footprint. Firms identified increasing interest rates, significant private equity capital entering the market, and more demand as an increasing number of players are competing for the same business, as some of the reasons for the change in EBITDA multiples compared to three years ago.

The survey was fielded from February 13 through March 28, 2023, and covered M&A deals between January 2020 and March 2023. Twenty-six RIAs and four COI (Center of Influence) firms participated in the survey. The 2019 study covered M&A deals between January 2017 and July 2019. Twenty-three firms participated in the study.