A newly released survey of plan sponsors reveals that many continue to broaden efforts to help participants achieve retirement security across employee financial wellness, plan design, and increasingly—retirement income.

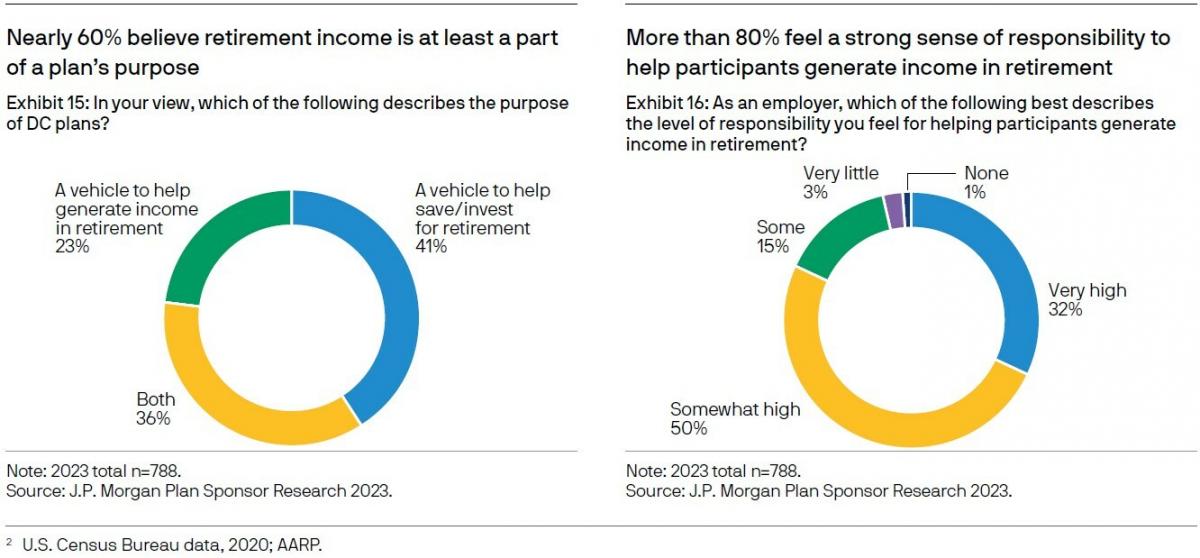

Findings from J.P. Morgan Asset Management’s fifth survey of U.S. defined contribution (DC) plan sponsors show that nearly 60% believe retirement income is at least a part of a plan's purpose. And more than 80% feel a strong sense of responsibility to help participants generate income in retirement.

Findings from J.P. Morgan Asset Management’s fifth survey of U.S. defined contribution (DC) plan sponsors show that nearly 60% believe retirement income is at least a part of a plan's purpose. And more than 80% feel a strong sense of responsibility to help participants generate income in retirement.

What’s more, 9 out of 10 "strongly agree" or "somewhat agree" that it is important to offer investments that help participants generate income in retirement. For plans without a current retirement income option, close to half (45%) say that they are "extremely likely" or "very likely" to consider offering one in the upcoming year.

J.P. Morgan notes that, similar to many past DC plan innovations, this trend is being led by sponsors with a more proactive plan design philosophy. The “extremely/very likely” figure reported by sponsors in this group is 59%, compared with 29% for plans with a primarily participant-driven philosophy.

The survey of 788 plan sponsors and resulting white paper—titled Continued Progress through Partnership—draws on a decade of data tracking the evolution of DC plan sponsors' views and actions.

“Our enhanced 2023 plan sponsor survey highlights the industry shift as plan sponsors begin to recognize the interconnection of overall employee financial and personal wellness,” observes Alexandra Nobile, vice president of Retirement Insights at J.P. Morgan Asset Management. “Retirement income, student loan debt assistance and emergency savings programs are all being discussed more and it's exciting to see that companies offering these types of programs see their retirement plans as more effective."

Nobile further emphasizes that the implications of SECURE 2.0 serve to only accelerate this trend, as the firm expects to see more plan sponsors taking a proactive approach to evolving their retirement benefit offerings through innovative DC plan design.

In addition to the findings surrounding retirement income, results from the survey reveal three additional key themes.

Automation and Customization

J.P. Morgan found that automation and customization continue to gain momentum. To help drive stronger participant outcomes, more than 6 in 10 plan sponsor respondents (61%) indicate that they take a more proactive plan design approach, and a higher number of these plan sponsors view their plans as "extremely effective," or "very effective."

Moreover, there has been an increase in the number of plans that now offer automatic contribution escalation, with 43% of surveyed sponsors reporting this feature, up from 21% in 2013. Six percent indicated that they are unsure if they offer automatic contribution escalation.

Perhaps somewhat surprisingly, nearly half (47%) of surveyed sponsors continue to choose not to offer automatic enrollment in their plans (around 2% are unsure if they offer), and 51% do not offer automatic contribution escalation.

TDF Usage

Not surprising, however, is that target date fund (TDF) usage remains high as sponsors refine their investment menus. Here, the firm found that 6 in 10 plan sponsors offer a TDF in their DC plan, while 76% of sponsors with a QDIA say it is a series of TDFs.

The most frequently reported investment menu changes were "added an option designed to generate income for retirees" (45%), and "reducing the number of investment options" (35%). Around a quarter have changed their plan TDF suite and/or their qualified default investment alternatives (QDIAs).

Meanwhile, three out of four surveyed sponsors report feeling "extremely confident" or "very confident" that their participants have an appropriate asset allocation, led by proactive sponsors at 85% versus 59% for sponsors with a participant-driven philosophy.

Proactive sponsors are described in the study as those that actively implement programs that make it easy to tap into the benefits of the plan, such as automatic enrollment and contribution escalation, personalized communications, and investment defaults into TDFs and other professionally managed asset allocation strategies.

The increasing popularity of reenrollment may also be playing a part here, with 55% of plan sponsors having considered reenrollment, and more than a quarter having already conducted or planning to conduct a reenrollment in the next 18 months (up from 7% in 2019).

Notably, only 55% of surveyed sponsors know that they serve as a fiduciary, even though all the respondents have fiduciary responsibilities, the study further observed.

Financial Wellness Responsibility

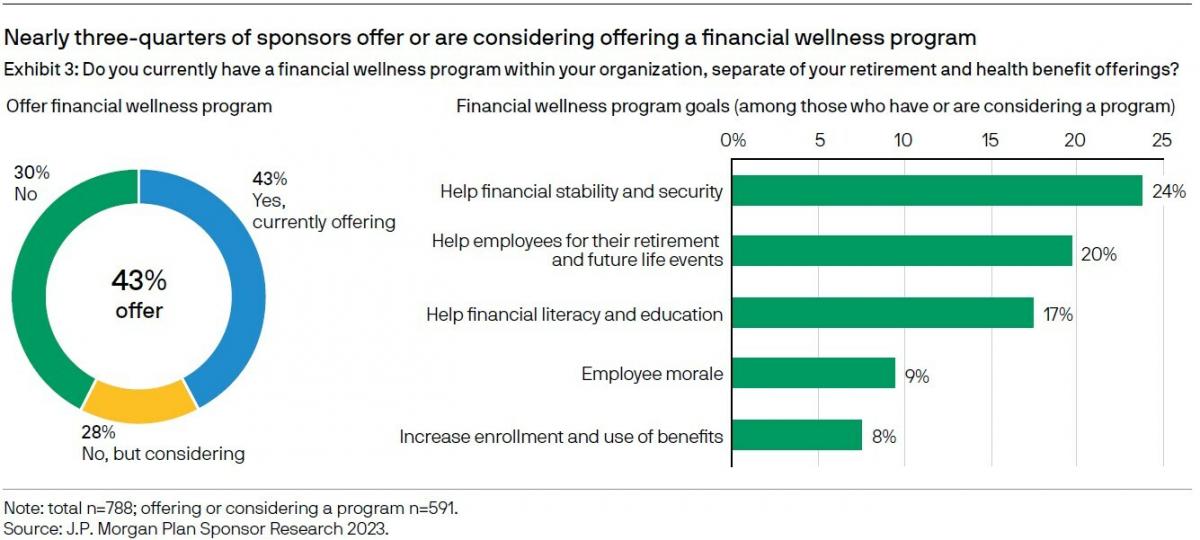

J.P. Morgan also found that nearly three-quarters of plan sponsors offer or are considering offering a financial wellness program, and 85% feel a strong sense of responsibility for employee financial wellness, up from 59% in 2013.

Additionally, sponsors with a financial wellness program more often see their retirement plans as effective in meeting key goals, compared with those without such a program. In this case, 95% believe they are helping make sure employees have a financially secure retirement, the study shows.

And in an increasingly tight labor market, employee benefits are top of mind, as more than 7 out of 10 respondents report offering employees life insurance, 6 out of 10 offer disability insurance and mental health benefits, half make health savings accounts (HSAs) available, and just under half provide paid parental or caregiving leave. These numbers grow even bigger for larger plan sponsors, with more than $250 million in plan assets.

In addition, a quarter (25%) of surveyed sponsors offer student loan debt assistance, and 40% offer emergency savings benefits, one-on-one financial coaching and/or debt management assistance.

Going Forward

With SECURE 2.0 in place, efforts to continually evolve financial wellness offerings, as with other areas of retirement benefits design, will be beneficial for both participants and plan sponsors, the firm suggests.

"Our research shows that DC plans have become the primary retirement savings vehicle for most working Americans, and in many ways plan sponsors have risen to the occasion, however there is a clear need for plan sponsors to better understand their role as a fiduciary, with just under half aware of their responsibilities," emphasizes Catherine Peterson, Global Head of Insights & Product Marketing, J.P. Morgan Asset & Wealth Management. "We expect to see a continued emphasis on incorporating retirement income solutions into DC plans going forward having been identified by plan sponsors as a core purpose of plans."

The survey of 788 plan sponsors was conducted from Jan. 9–Feb. 28, 2023, in partnership with Greenwald Research. All respondents are key decision-makers for their organizations' DC plans. All organizations represented have been in business for at least three years and offer a 401(k) or 403(b) plan to their domestic U.S. employees.