One of the optional provisions in the SECURE 2.0 Act that some employers were very excited about is the provision to allow a 401(k) match based on a participant’s student loan payment rather than deferrals.

This was seen by many as a way to help young (or not so young) employees start saving for retirement while paying off loans—as student loan payments often force employees to delay saving for retirement until they are more financially secure. The excitement about this provision is highly variable across industries—many do not have a workforce that has student loans, while other industries do and see this as a great way to add value and recruit top talent in a tight labor market.

This was seen by many as a way to help young (or not so young) employees start saving for retirement while paying off loans—as student loan payments often force employees to delay saving for retirement until they are more financially secure. The excitement about this provision is highly variable across industries—many do not have a workforce that has student loans, while other industries do and see this as a great way to add value and recruit top talent in a tight labor market.

This provision is now effective (as of Jan. 1, 2024) and though our surveys last year showed that a handful of companies were moving forward with implementing it, most were focused on the mandatory provisions of SECURE 2.0 and/or waiting for some of the technical complexities to work themselves out.

Now that this provision is effective and companies have had a year to think about it, and we are expecting an initiative from the White House on student loans that may spur guidance on this, we asked companies where they currently stand on this provision and what guidance, if any, they would like from Treasury.

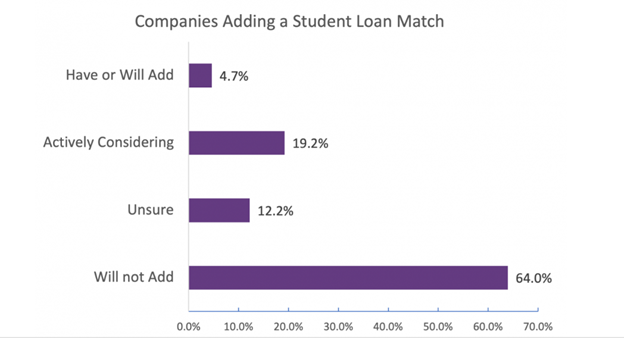

At this time last year, two-thirds of respondents were not planning on adding this feature with only 12% likely to implement it. When asked in September 2023 which of the optional provisions that members were planning to implement, 3% stated they were planning to implement the student loan match with 30% still considering it.

At this time, 5% have implemented this program or will implement it this year with 20% currently considering it, and 12% unsure. That leaves nearly two-thirds that are not, and will not, implement this provision.

Source: PSCA

When asked about what guidance from the Treasury Department they would like to see before making a decision about this provision or before implementing it, the responses varied from technical questions, such as how to track employees’ student loan payments, to regulatory questions, such as how this would work with safe harbor plans, to not waiting on guidance but just waiting to work out the technical complexities with their providers. Select comments follow.

Added/will add:

- How to verify loans.

- I would like a description of the processes and qualifying repayments.

- No, we went live with enrollments in early November and loan tracking starting Jan. 1, 2024.

Considering:

- I would like any information I can get. Working with my broker to decide if this is worth the hassle. Kind of just waiting to see what others are doing as well.

- More information about how the verification process will work for the plan sponsor. Will it be participant certification? Can the plan sponsor ask for proof? Does the sponsor have a specified period in which they need to deposit the match. How long will providers have to ready their systems for compliance?

- No, it's about economics. we may add in the future

- No. Just trying to decide.

- No. We are looking at whether it would be valuable for our employee population. Most of our employees do not pursue or have higher education.

- Requirements for proof. Need a recordkeeper who can track the loan payments and coordinate the match so we don't have an additional administrative burden.

- Secure 2.0 indicates that the participant can self-certify that they have made loan payments. We need to know if, as the employer, that we can require proof of payment of if we must allow the participant to self-certify.

- Tax implications

- The complexity of administering this between loan recordkeepers and 401(k) recordkeepers and any consequences for incorrect information/reversals.

- This would be administratively challenging to manage. Our 401(k) match is automatically calculated and sent to our recordkeeper each payroll. This process would have to be manual since there is no 401(k) deduction in the payroll system for it to calculate the match.

- We plan to implement, but are waiting for guidance before we do so.

- We would want to know how the payment to the student loan would be submitted - through payroll, through the 401(k) plan, or a different method.

- Would like to see that the match will not impact NDT.

- Yes, and waiting on our retirement plan provider to update us on the updated guidance.

Will not add:

- At the moment, it is considered too complicated to implement.

- At this time we will not be contributing a 401 match based on student loan payments. We will add this feature if it becomes mandatory.

- Brought it up at committee and there is no interest. Majority of our population is unskilled labor.

- compliance and documentation nightmare.

- Does this apply to 403b plans?

- How difficult would this be for employers?

- No—but always curious....

- NO—emphatically NO!

- No—it is fundamentally inconsistent with our benefits philosophy

- No—our plan already provides above-market company contributions for a minimal (2%) employee contribution. This allows them to allocate elsewhere money that they might have needed to obtain a full company match.

- No, as a governmental plan, the State legislature would need to pass legislation to permit this change. There has been no interest in the legislature thus far.

- No, we as a company have decided not to add this option due to our plan designs and additional administrative requirements.

- No, we do not intend to adopt this provision.

- No, we don't currently offer a match so we would add a 401(k) match before adding a student loan payment match.

- No, we have an external student loan repayment program and are not considering adopting this provision.

- No. It just isn't something we feel we need for our workforce.

- No. We are a masonry contractor - most employees do not have student loan payments.

- No. We are not adding this provision regardless.

- Not at this time. We have other priorities.

- We are a small company with a safe harbor plan.

- We don't have a match. We have a profit sharing plan - lump sum at end of year placed into participant accounts.

- We have a safe harbor plan, not a matching plan, so I don't think we can implement.

- We haven't received significant request for this nor consider it a proper use of 401k funding.

- We would be happy to provide such a benefit if there was not an additional administrative cost from a TPA.

- Yes, would like to know if we can set up a diff match % or flat $$ than that avail to our actively participating EEs.

Unsure:

- Determining logistics internally.

- No. If our company implements 401K match, then we will add student loan payments

- Not sure that all parties involved are ready and able to handle this yet

- Our issue is more that most of our employers don't offer a match, so we likely will not implement because the number of people who would actually be able to take advantage are quite small. But we do like that there are more options for people to pay down student debt and still save for retirement. Just not that applicable to our plan.

- We do not currently plan to add but that may change in the future.

- Would like to know exactly how we are supposed to know how much was paid by the employee on student loans.

- Yes, would like to understand more about it before making the decision.

Hattie Greenan is Research Manager for the Plan Sponsor Council of America.