Are you doing more business with – and through – third party administrators? If so, you’re not alone.

Advisors participating in the nation’s retirement plan advisor convention brought a lot to the sessions, networking, and – once again, shared valuable insights via an exciting new medium: the NAPA 401(k) SUMMIT Insider.

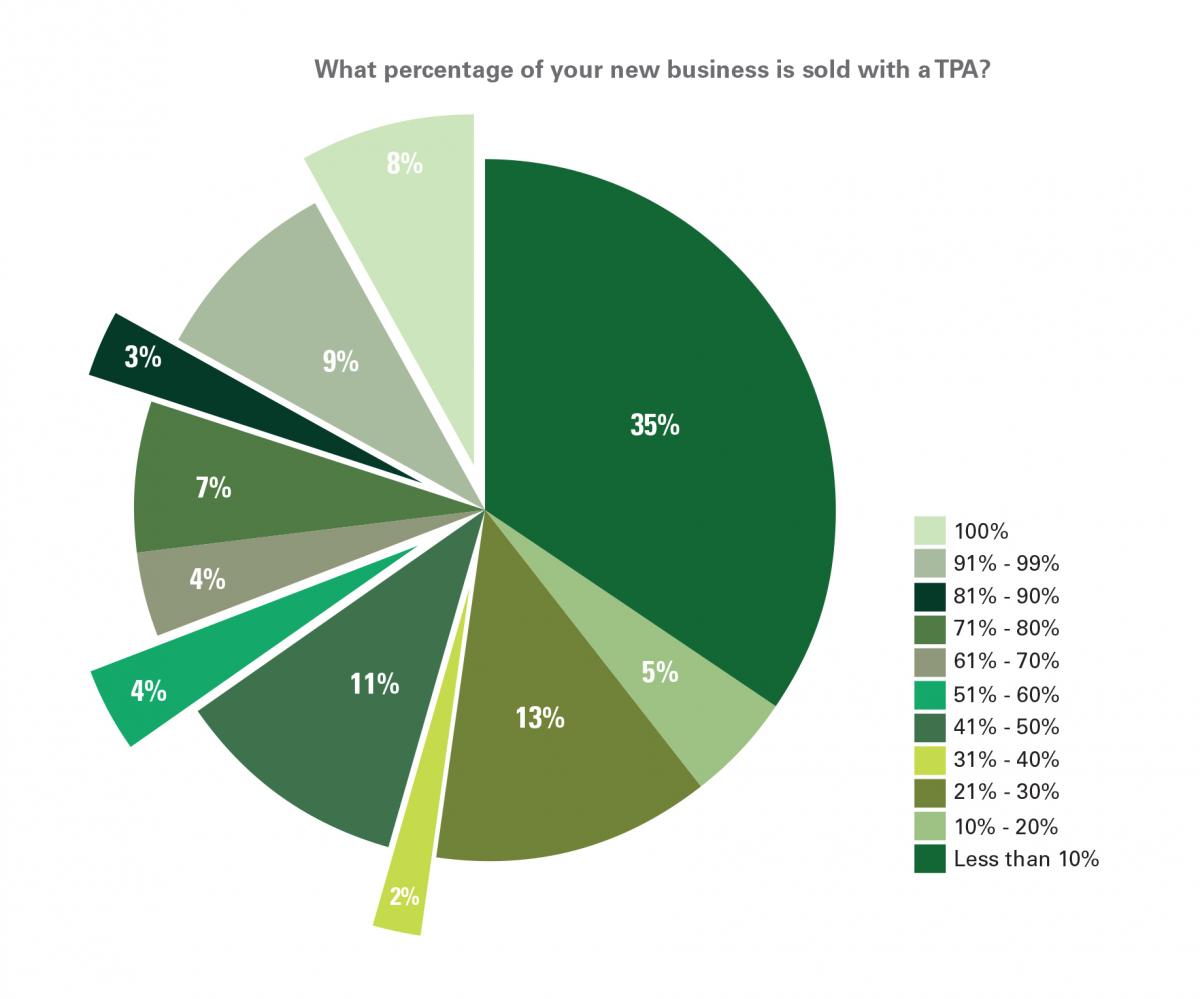

A new question this year had to do with third-party administrator relationships, specifically what percentage of their new business was sold with a TPA.

Of course, the “third-party” harkens back to a realization that these firms, as with recordkeepers generally, provide services to a plan sponsor that plan sponsors once did for themselves. Things have grown significantly more complicated over the years, though and today TPAs not only keep up with participant accounts, they can be an invaluable resource to plan sponsors – and advisors – on issues like regulatory compliance and plan design.

We’re talking about an extraordinarily extensive list of services, including amending and restating plan documents; preparing employer and employee benefit statements; assisting in processing all types of distributions from the plan; preparing loan paperwork for plan participant; testing the plan each year to gauge its compliance with all IRS non-discrimination requirements as well as plan and participant contribution limits; allocation of employer contributions and forfeitures; calculating participant vested percentages; and preparing annual returns and reports required by IRS, DOL or other government agencies.

A TPA can be a plan advisor’s best friend. But it’s important to understand the various types of TPAs and how to best leverage them depending on the plan profile and size.

Roughly a third (35%) of this year’s respondents sold more than half of their new business with these partnerships, and nearly one-in-ten (8%) have relied on these relationships for 100% of their new business.

But as you can see on this chart, the results were quite varied.

And yes, while those primarily focused on plans with less than $5 million in assets were significantly more likely to do 100% of their sales via TPAs (they were more than half that group), they didn’t have a monopoly on that level of commitment. Roughly 10% of the advisor respondents that did at least 90% of their business with/through TPAs focused on plans with at least $250 million in assets.

Next: Top Recordkeeping Selection Criteria