One of the great concerns of our industry—when we aren’t worrying if people have saved enough for retirement—is worrying about how those savings are going to be enough to last through retirement. In this year’s Summit Insider, we asked attendees at the 2021 NAPA 401(k) Summit to weigh in on the issues—and solutions.

One of the great concerns of our industry—when we aren’t worrying if people have saved enough for retirement—is worrying about how those savings are going to be enough to last through retirement. In this year’s Summit Insider, we asked attendees at the 2021 NAPA 401(k) Summit to weigh in on the issues—and solutions.

There’s little question that participants need help structuring their income in retirement—and little doubt that a lifetime income option could help them do that. That said, the biggest impediment to adoption may simply be that (industry surveys notwithstanding) participants don’t seem to be asking for the option—and when they do have access, mostly don’t take advantage.

As part of this year’s Summit Insider, we asked advisors (approximately 525 responded) the following:

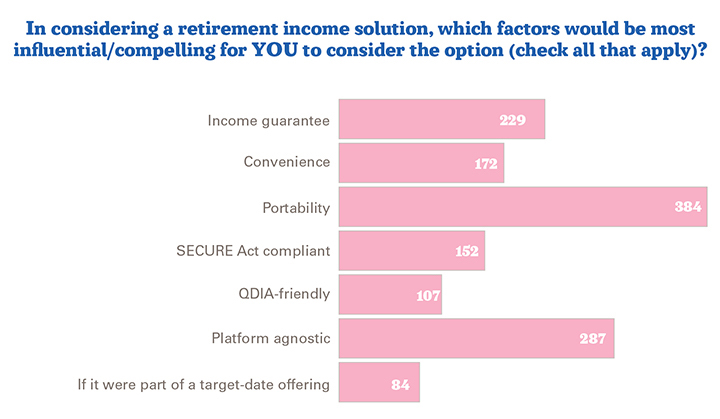

In considering a retirement income solution, which factors would be most influential/compelling for YOU to consider the option? (More than one response was allowed.)

229 - Income guarantee

172 - Convenience

384 - Portability

152 - SECURE Act compliant

107 - QDIA-friendly

287 - Platform agnostic

84 - If it were part of a target-date offering

In considering a retirement income solution, which factors would be most influential/compelling to your plan sponsor clients/prospects? (More than one response was allowed.)

281 - Income guarantee

258 - Convenience

313- Portability

155 - SECURE Act compliant

95 - QDIA-friendly

200 - Platform agnostic

59 - If it were part of a target-date offering

Which guaranteed retirement income features do you think would be most appealing to participants? (More than one response was allowed.)

385 - Income guarantee

202 - Convenience

287 - Portability

218 - Flexibility

Ultimately, these results indicate that while there are overlapping preferences to resolve some of the take-up resistance, portability seems to loom largest as a concern of advisors and plan sponsors (at least how their advisors see it)—and it’s also a high priority for participants.