Plan sponsors need to understand the financial readiness status of each plan participant in their workforce.

Recently, the Board of Governors of the Federal Reserve System disseminated a letter of review of the regulatory investigation conducted on Silicon Valley Bank (SVB). That oversight letter, dated April 28, 2023, was penned by Michael S. Barr, the Vice Chair for Supervision at the Federal Reserve System.

Recently, the Board of Governors of the Federal Reserve System disseminated a letter of review of the regulatory investigation conducted on Silicon Valley Bank (SVB). That oversight letter, dated April 28, 2023, was penned by Michael S. Barr, the Vice Chair for Supervision at the Federal Reserve System.

The document[1] includes:

- four key takeaways;

- a 14-page executive summary;

- a 12-page description of Federal Reserve supervision; and

- a six-page compilation of lessons learned and issues for consideration.

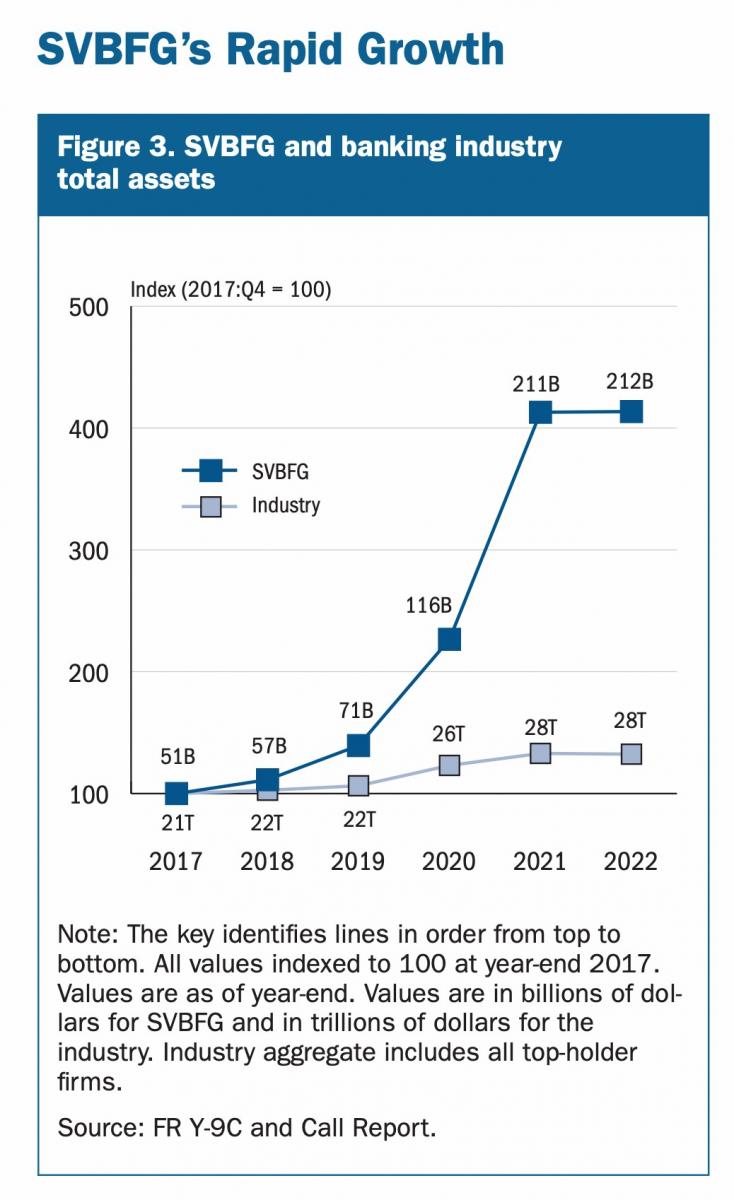

The above topics and more are wrapped up succinctly in 118 pages. However, what really caught this reader’s eye are two charts and the path to the disaster that began in 2019.

The story has been silently developing for years. Then, suddenly, during the first quarter of 2023, we all had front-row seats to the SVB season finale. As the curtain lowered on the closing scene, the chorus sang a familiar tune, “What was the Federal Reserve thinking?” with background music played by Asleep at the Wheel.

Could there be a more alarming pair of visuals for bank governors and supervisors than these two charts? Bank governors and supervisors ignored these wake-up calls.

Today’s banking system quagmire leaves bankers, depositors, and the public, in a state of disbelief, over regulators who waited too long to regulate.

What might the SVB banking debacle have to do with qualified retirement plans? It all comes down to proper oversight.

Enter Private Retirement Plans and Fiduciaries Who Watch Them

As de facto regulators, plan sponsors and retirement plan advisors are the first lines of oversight of qualified retirement plans. Fortunately for plan sponsors and advisors, there are reports and charts—like those above—that can serve as early warning systems to help fiduciaries identify the challenges and shortcomings of a retirement plan.

However, plan sponsor fiduciaries may require the assistance of a knowledgeable plan advisor to locate such information. Fiduciaries must know where to look for this valuable information.

Read more commentary from Steff Chalk here.

What Can Fiduciaries Learn from the DOL?

Plenty. Plan sponsors can never be sure of what an auditor is looking for since the audit function and the auditor’s intent are not exact sciences. What can be known, with reasonable certainty, is what the auditors have “found” during prior audits.

For plan fiduciaries, it is all about making prudent decisions. To that end, I recommend the following three web addresses, which cover DOL Documented Violations, a DOL Enforcement Update, and What to Know During a DOL Investigation.

- DOL: Example Violations Applicable to both Pension and Welfare Plans

- Morgan Lewis: DOL ERISA Retirement Plan Enforcement 2022 Update

- Faegre Drinker: 20 Items You Should Know About DOL ERISA Investigations

Road to Retirement Reporting

Plan sponsors need to understand the financial readiness status of each plan participant in their workforce. Today this means actively measuring how each employee stacks up in their quest for reaching retirement age with sufficient assets to retire.

Having a workforce that is “ready to retire” is dramatically different from simply offering employees a retirement plan.

The 2023 NAPA 401(k) Summit exhibit hall was populated with many providers willing to help plan advisors or plan sponsors with the creation of gap analysis reports. Doing so requires initiative, some census data, and the time to make it happen.

In the end, these reports are well worth the effort. Informing plan participants of their need to make changes to deferral amounts, investment allocation, anticipated years to retirement, or spending habits is a valuable employee benefit. The benefit is highly valued in the eyes of the plan participants.

But the plan sponsor and the TPA or recordkeeper need to be in-synch. Good advisors work tirelessly to make the requisite retirement-gap analysis reports available to plan sponsors and plan participants.

Just as in the case of SVB, possessing access to knowledge and failing to act upon it is a poor defense.

Steff Chalk is the Executive Director of The Retirement Advisor University (TRAU), The Plan Sponsor University (TPSU) and 401kTV. This column first appeared in the Summer issue of NAPA Net the Magazine.