There is certainly no doubt for a plan sponsor and a retirement advisor that one of the most impactful investment decisions being made today is determining the optimal QDIA for plan participants. As a result of the fiduciary duty to consider and evaluate all QDIA options, and a growing focus on delivering more personalization and opportunities for holistic advice, managed accounts are poised to finally have their moment.

The growing trend of advisor managed accounts, and the consensus view that managed accounts is the ideal method for delivering personalized recommendations to guaranteed income products, are nudging more plan sponsors to rethink the “default” default of off-the-shelf target-date funds.

When the current QDIA is a target-date fund, and it has served the plan well for many years, often a dynamic QDIA is explored and implemented. The plan sponsor and advisor can quantify the value of personalization and believe it is especially important, impactful, and warranted as participants age. Those of you that know me know that I am a big believer in managed accounts as the full QDIA.

I don’t understand how average is good enough in this circumstance, when we strive to be better than average in every other aspect of both our work and personal lives.

That said, our own data suggests that the dispersion from the mean, or the impact of personalization, can be more meaningful past age 45. An industry colleague of mine likes to say, “as we accumulate years, we accumulate differences.”

Adding to the buzz, many advisors and sponsors agree that a managed account service is the best delivery mechanism for general spending advice for participants. With the increased prevalence of guaranteed income solutions, having managed accounts as the default to deliver annuity recommendations to participants approaching retirement is becoming more and more of a focus.

Dynamic QDIA is here. Interest is up. Adoption is up. Product variation and innovation is occurring.

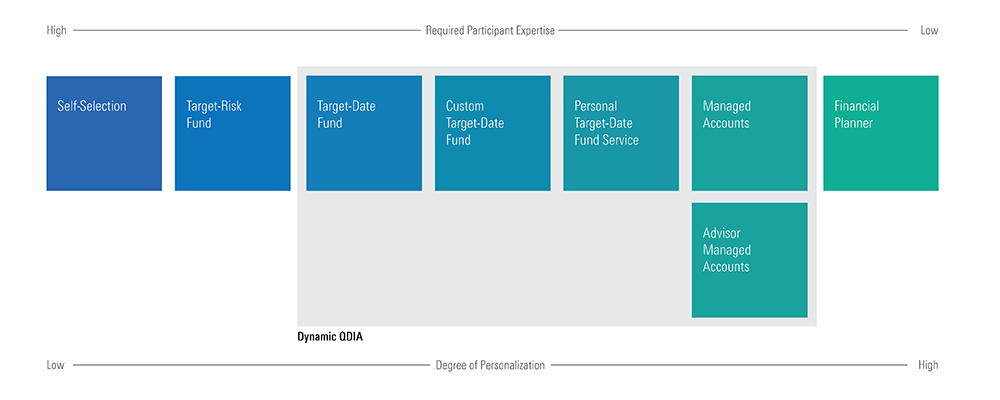

Caption: Dynamic QDIA offers a phased approach to personalization that combines TDF investments for younger participants with a transition into managed accounts for older participants. The dynamic QDIA model provides participants approaching retirement with more risk-appropriate portfolios personalized to their dynamic circumstances without the need for engagement by leveraging data sourced from the recordkeeper.

The two big questions when a sponsor and advisor decide to implement dynamic QDIA:

- What solution is up front for the younger participants?

- What age should they select to transition to managed accounts?

Morningstar Retirement helps with No. 2 everyday by providing guidance and analytics for plans and advisors to dig into the demographics of plan participants, so let’s focus on question No. 1: what’s up front?

I’ll provide a summary of the options available today, and the pros and cons I see across the set of alternatives.

Off-the-Shelf Target-Date Funds

A natural place to start for the sponsor and advisor, but honestly, I think we can all do better. The statement I hear most from a plan sponsor or advisor who is explaining why they are using an off-the-shelf target-date fund as the first half of the QDIA is: “It was already in the plan as the QDIA, and it is very low cost (very often all passive), so it made sense.”

When they say that, a cartoon dialog box, only visible to me, appears above me. In it, Larry David giving a shoulder shrug and saying, “meh.” It makes me a little sad, but then I remind myself this is a better alternative than what they had before, and I move on.

This is a good option, an improvement. In my experience, low cost, familiarity, and simplicity are the three main drivers when using an off-the-shelf TDF on the front end.

The choice does bring to light a few key concerns—philosophical mismatches, if you will.

- Two distinct glide path and asset allocation methodologies across the TDF and managed account services. This can feel like a jumbled mess at times, and can create abrupt, inconsistent transition from TDF to managed accounts. Different views on asset classes, a different set of included asset classes, different demographic and capital market assumptions that drive the glide path methodology.

- Not leveraging the core menu creates questions – Is cost the singular concern, over all else? Why even have a core menu if you aren’t going to use it? Is the core menu right for older participants but has no value for younger participants?

If the plan has an all-passive core menu that reflects the underlying funds used in the target-date series, this is a moot point and would create a smoother transition and experience for participants.

- Piling on with the classic we all love, the active vs. passive debate – If you:

- Have built a core menu of well thought out active and passive investment options

- Are using a passive TDF as the front end of a dynamic QDIA

- Use managed accounts as the back end of the dynamic QDIA, leveraging all options the fiduciaries have chosen to include in the plan

Then you are essentially taking the position once again that cost is the only consideration, and that only older participants receive value in a well-thought-out mix of active and passive investments. No more piling on, but this one is a head scratcher.

Recordkeeper Custom Models

For many years, recordkeepers have had asset allocation programs that have allowed plan sponsors and advisors to build a set of custom models using the templated asset allocation framework and the core menu. Those programs have evolved over the years to reflect a target-date or glide path approach, versus the more traditional risk-based model construct. They make a great option as the “TDF” component in a dynamic QDIA.

Depending on the fiduciary duty and complexity, these custom model programs can be anywhere from free or included in the recordkeeping cost (most often non-fiduciary), to a few basis points for 3(38) or 3(21) programs.

Custom model programs improve upon the off-the-shelf TDF option in a couple of ways. The core menu is often fully leveraged, creating consistency of asset classes and fund specific building blocks across the full QDIA. That also helps take the active vs. passive debate off the table, with usage across the full age spectrum.

One added benefit, Morningstar Investment Management is often the consultant, sometimes even the fiduciary, for many of the recordkeepers’ custom model programs. As a result, asset allocation methodologies may have some consistency across the full QDIA.

The drawbacks can be twofold. First, I want more personalization. Many of these programs often don’t consider participant or plan demographics when creating the asset allocation, but rather leverage a simpler risk-based glide path construct, where nearly every plan uses the “moderate” option.

Second, there can be some asset class rigidity, or requirements, that can sometimes feel like jamming a square peg into a round hole. High quality advisors have been navigating that successfully on behalf of their clients for years, but it is something to be mindful of.

Custom Target-Date Funds

Custom target-date funds have been very popular in the large and mega market for many years, and are in many ways, a near perfect front end to a dynamic QDIA. Custom target-date funds take many of the mismatches I highlighted prior completely off the table and can make considerable improvements on the personalization front. Two such improvements are the use of the core menu and the ability to align fund specific and active/passive viewpoints across the full QDIA.

Custom target-date funds can also create plan level personalization of the glide path and asset allocation methodologies, leveraging participant demographics and plan level data to develop optimal glide paths and asset allocations for the front end of the QDIA. If an off-the-shelf glide path is using data about the average American worker, a custom TDF is using data about the average 401(k) participant at the employer.

When methodologies and investment implementation are aligned across the TDF and the managed account, the transition is seamless and can feel like a single QDIA from front to back.

Custom target-date funds are often constructed by the current retirement advisor working with the plan sponsor, or a third-party fiduciary like Morningstar Investment Management. In the same way we help recordkeepers design custom model services, today we work with many large plan sponsors to build custom TDF services.

We also help power some of the custom TDF programs for retirement RIAs, helping them scale to meet the needs of their plan sponsor clients, across plan sizes. From a dynamic QDIA perspective, having the same methodology driving, or at least informing, can create a very cohesive, easy-to-understand, and easy-to-implement strategy.

A very recent innovation is happening now, as more and more RIAs are exploring dynamic QDIA services. In a typical advisor managed account, the retirement advisor builds a core set of portfolios, and the platform provider scales and blends those portfolios to deliver personalized recommendations to plan participants.

That same construct can be used for the custom target-date fund portion, using the core portfolios as the building blocks, and personalizing to the optimal portfolio for the given age cohort. The result is a dynamic QDIA with a uniform strategy across all age cohorts, and both custom TDF and managed accounts users.

We believe custom target-date funds could become the best practice in dynamic QDIA implementation, but it does have a couple of minor drawbacks. First, it has to be managed. For a plan sponsor looking to simplify, this does add some complexity to your fiduciary duty. Second, there is often an additional cost to custom TDF implementation, often in the low single-digit basis points. However, in a dynamic QDIA setting, we’ve seen those expenses be lower and often zero.

Personalized Target-date Funds

In the last couple of years, personalized TDFs have taken off. An innovative QDIA solution coming from asset managers who have had successful off-the-shelf TDFs for years, personalized TDFs attempt to fill the gap between an off-the-shelf TDF and a full-service managed account program.

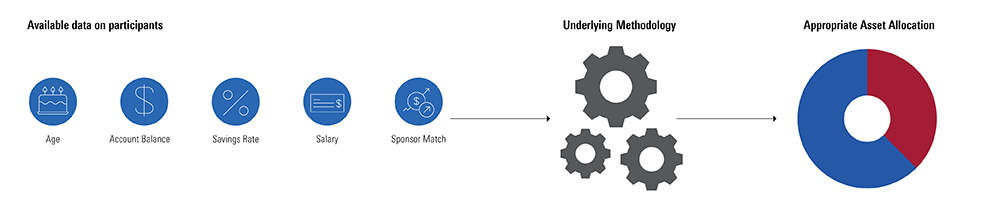

In general terms, the solution gathers the basic data points available on the recordkeeping platform: participants’ age, salary, savings rate, employer match rate, and account balance.

They leverage this data and underlying methodology to make an optimal investment recommendation, implemented by blending two of the asset managers’ off-the-shelf TDFs at the appropriate percentages to achieve the target. In short, it is an optimal blend of two TDFs to achieve a more personalized and risk-appropriate investment recommendation than a single TDF.

As a QDIA, personalized TDFs have been slow to take off, but we see some signs of growth in 2024. Ascensus recently announced the launch of a PEP with Capital Group, which will feature the American Funds Target-Date Plus, one of the leading personalized TDF solutions. We know of a few recordkeeping platforms that will be adding both American Funds Target-Date Plus as well as the other leading option today, PIMCO myTDF.

We still have a way to go before personalized TDFs are a common choice as the full QDIA, but as the front end of a dynamic QDIA, I see application in the near-term. If the product has glide path and investment methodology alignment with the managed account service, a personalized TDF could offer the highest degree of personalization among any of the “front end” choices for dynamic QDIA.

A couple of tradeoffs occur because of the additional level of personalization. First, you sacrifice leveraging the core menu, which creates the mismatches in asset class availability and active/passive expression that I highlighted as concerns with regular off-the-shelf TDFs.

The second is fee compression in the managed accounts space, which has the potential to close the fee gap between TDFs and managed accounts, which could make it difficult for personalized TDF solutions from a cost perspective, as the basis point fee typically sits in between TDF and managed accounts.

Conclusion

Dynamic QDIA across the industry is coming, and for those recordkeepers like Empower who embraced it early, it has been here for a while now. We are excited about it and believe dynamic QDIA provides better outcomes than standalone TDFs. Dynamic QDIA is a big step towards expanded use of personalization.

The ability to implement the TDF portion of the solution in various ways, based on the sponsor and advisor's desires, is good. The preferences of the plan sponsor around cost, leveraging the core menu, methodology alignment, and the level of personalization are all factors that can be quantified and evaluated, with the help of a retirement plan advisor.

Last words: do the exploration. Go through the QDIA selection process; there is a whole spectrum of options beyond the “default” default.

Nathan Voris is Head of Channel Strategy for Morningstar Retirement.