A danger when retirees can least afford it is an ill-timed, significant loss occurring immediately after they begin plan distributions.

Plan sponsor trustees hold the “power seat” for retirement plan participants by providing oversight for plan investments. It’s seen in the names, titles, and job functions historically cited in fiduciary breach lawsuits. ERISA comes with rules, regulations, and a rudimentary roadmap. When a plan fiduciary lacks the required knowledge to serve as an ERISA fiduciary, it creates a fertile hunting ground for lawsuits. Fortunately, regulators largely support plan fiduciaries engaging prudent professionals when they lack the requisite expertise.

Plan sponsor trustees hold the “power seat” for retirement plan participants by providing oversight for plan investments. It’s seen in the names, titles, and job functions historically cited in fiduciary breach lawsuits. ERISA comes with rules, regulations, and a rudimentary roadmap. When a plan fiduciary lacks the required knowledge to serve as an ERISA fiduciary, it creates a fertile hunting ground for lawsuits. Fortunately, regulators largely support plan fiduciaries engaging prudent professionals when they lack the requisite expertise.

After a retirement committee engages a team of experts to orchestrate the plan’s duties, it seems all appropriate boxes are checked. An inexperienced plan fiduciary may feel there is not much left to do. However, retirement planning goes well beyond the accumulation period.

Once prudent processes are defined and followed, and appropriate funding mechanisms are in place—there remains an all-encompassing next step.

Getting People Ready to Retire

The task at hand in retirement is building upon the past good work of plan sponsors, plan providers, fiduciaries, and advisors for the past 20 or 30 years. The challenge then becomes structuring that asset into one that can best deliver the participant through whatever life might throw at them.

A retiree’s final 20 years of retirement living is far less clear or structured than during the accumulation period. To assist plan sponsors and plan participants during the decumulation period, there are a few macro-concepts of which the retiree should be aware, beginning with inflation.

Inflation

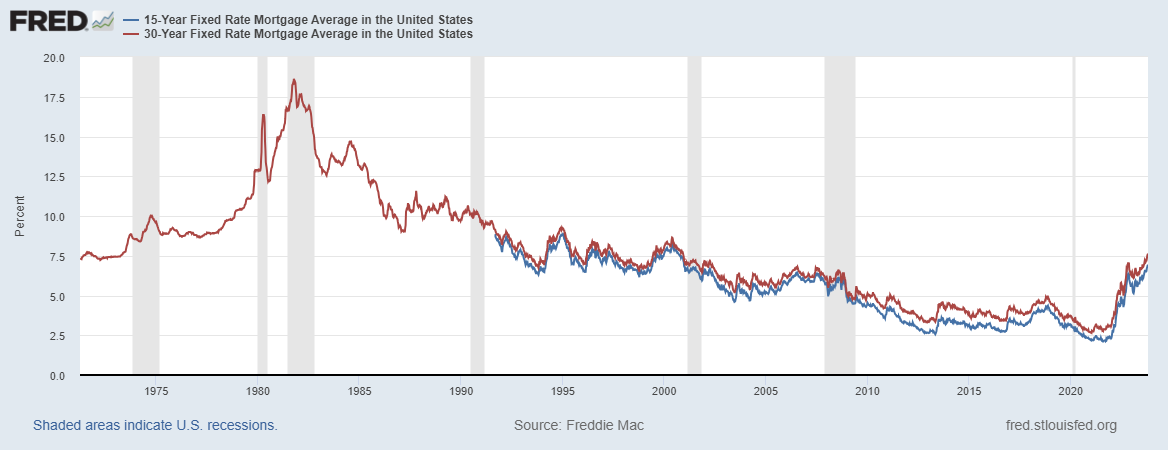

Inflation needs no explanation for those who can recall the Carter and Reagan Administrations. Consumers and borrowers in the 1980s can remember residential mortgages peaking at over 18.5%. Inflation can still be defined simply as the erosion of a currency’s buying power.

Source: “What’s the story with mortgage rates?” fredblog.stlouisfed.org.

Retirees must be aware of inflation’s impact on their existing portfolio. One individual cannot stop inflation. However, one good advisor can periodically perform a stress test on a client’s portfolio to provide a retiree with a clear understanding of the impact inflation could have on their portfolio.

Read more commentary from Steff Chalk here.

Asset Allocation Surprises

Many retirees maintain a substantial amount of financial assets committed to equity securities. Unfortunately, equities can reprice instantaneously with an unfavorable earnings report that drives a market selloff or with deteriorating global conditions in general. A large drop would not be devastating if a retiree holds only 5% of their post-retirement portfolio in equities. However, if a considerable portion of a retiree’s retirement assets are held in equities, then discussions around diversification, correlation, and downside protection become more pertinent. In most cases, a retiree will not think that far ahead, but a good retirement advisor will.

Sequencing-of-Returns—Does It Matter?

Another danger that creeps into a portfolio when retirees can least afford it is an ill-timed, significant loss occurring immediately after they begin plan distributions. Spending-down/withdrawal modeling is normally computed with asset allocation ranges and average return assumptions. Yet, what is not normally built into the model is a significant loss—or a series of losses—in the portfolio during the first few years of retirement. A substantial loss during the early years of retirement can profoundly impact the following 10 or 20 years. If sequencing of returns is not in your lexicon, Moshe Milevsky’s articles on the subject should be both eye-opening and required reading.

It’s not the returns that are the problem; it’s the timing. Taking 4% withdrawals with multiple years of negative returns in the portfolio can be a significant issue.

By keeping their eyes open to portfolio risk, seasoned retirement advisors who maintain plan participant relationships beyond the qualified plan can consistently be of great value and service to a plan sponsor’s employee base.

Steff Chalk is the Executive Director of The Retirement Advisor University (TRAU), The Plan Sponsor University (TPSU) and 401kTV. This column first appeared in the Fall issue of NAPA Net the Magazine.