One of the simplest investment options for the average DC investor, and one that can be very effective in achieving long-term retirement goals, is the good old target-date fund. Unfortunately, as two decades of research has shown, investors who truly understand TDFs and their intended purpose are in the distinct minority.

A target-date fund is, by design, a highly diversified investment that has been optimized to minimize risk and optimize returns based on an individual’s investment time horizon (i.e., retirement date). It serves as a single, all-in investment solution.

Yet the majority of DC investors who are offered TDFs only “partially invest” in them. According to a recent study:

Part of the appeal of target date funds is that they are designed to be an all-in investment. However, fewer individuals use TDFs as their sole investment than use TDFs in conjunction with other funds — 49.7% compared to 50.3%. (“Target Date Funds: Who is Using Them and How are They Being Used?”, Alight, 2017)

A finding of this same study points to the reason for this poor adoption rate: “When employees were asked about the features of TDFs, only 9% correctly understood that a TDF is designed so that investors need to invest in one fund instead of several funds.” Stated differently, 91% of DC investors believe that a TDF is just another investment fund like any other single asset class fund. This statistic alone could explain the reason why the majority of TDF investors are not fully invested in a single TDF.

Another study (“Not so Simple: Why Target-Date Funds are Widely Misused by Retirement Investors,” Financial Engines, 2016) reached similar conclusions, reporting that “the majority (58%) of retirement investors are not invested in TDFs. Of those who use TDFs, only one in four are full-TDF users.” Furthermore, in this same study, the number one reason (62%) given by partial TDF investors for not fully investing in a single TDF was that “they were seeking to diversify their investments.”

Communication Challenges

What these numbers illustrate is that, as in the ’80s and ’90s, plan sponsors (and their advisors) have mostly relied on “education” to achieve results. Before the advent of TDFs, the goal was to create sample asset allocation models for different risk profiles and hope that DC investors “got the message” and created (and managed over time) their own asset allocation models.

While it took a number of studies to prove that educating DC investors to perform asset allocation simply did not work, many plan sponsors and their advisors believed that TDFs would solve this education challenge. Simple, right? All the participants need to know is the date they want to retire and then choose the TDF that corresponds most closely with that date. Given the poor adoption rates of full TDF users, obviously this “simple” message is not getting through.

Click here to read more commentary from Jerry Bramlett.

Could it be that communicating TDFs as a single-solution fund is actually part the problem? As cited above in the Financial Engines study, more than half of the partial target-date investors were seeking to diversify their investments. Respondents in this study made comments such as, “You never know what could happen and I don’t want all my money in there [the TDF]” and “I do not like having all my eggs in one basket.”

Another of the study’s findings helps to explain why TDFs are widely misused: More than half of all partial TDF users (51%) and all retirement investors (60%) do not believe that TDFs can give them a better return than they can get on their own! This is an interesting conclusion, especially given that this same study demonstrated that partial TDF users had a 2.11% lower return than full TDF users did.

Increasing TDF Adoption Rates

Of course, many of the current studies and observations focus on shifting away from TDFs and moving on to managed account solutions or robo-advice. There are definitely merits to these arguments. Nevertheless, the fact remains that more than 90% of DC plans (at least across the top 100 plans, according to the 2017 Alight study) utilize TDFs as their core asset allocation option for participants. Furthermore, a study by Vanguard (“TDF adoption in 2016”) projects that by 2021, 65% of all Vanguard participants will be invested in TDFs, compared to 46% in 2016. That is a projected growth of almost 50% over a five-year period. This same study indicates that 80% of Vanguard plans have designated a qualified default investment alternative (QDIA) and of these plans with a QDIA, 96% have designated TDFs as their default option.

And yet the message — that best practices advocate for the use of a single TDF — continues to be lost on the average DC investor.

Better Choice Architecture: The Path to Success

Framing investment choices differently can make a difference in the investments chosen. An important study rooted in behavioral finance describes choice architecture in this way:

We show that the design of retirement saving vehicles has a large effect on saving rates and investment elections, and that some of the minor details involved in the architecture of retirement plans could have dramatic effects on savings behavior. We conclude our paper by discussing how lessons learned from the design of objects could be applied to help people make better decisions, which we refer to as “choice architecture.” (“Choice Architecture and Retirement Saving Plans,” Shlomo Benartzi, Ehud Peleg and Richard Thaler, 2007)

The worst possible choice architecture as it relates to the uptake of TDFs is to place these all-in-one funds alongside single asset class funds in the same menu. When TDFs are simply listed as a part of a fund lineup (which, unfortunately, is the case more often than not) the presumption is that participants will study the investment literature and understand the difference.

However, the cold, hard fact is that most participants do not read their plan’s investment materials. Instead, they take a look at the fund lineup and simply guess, based on how they feel about funds, or whether the choices are conservative, aggressive or diversified. Of course, many of these investors are lost, without knowing they are lost.

The best choice architecture is one that makes a clear distinction between a TDF, which is a well-diversified goal orientated fund, and a single asset class fund, whose purpose is to serve as one building block of an asset allocation strategy.

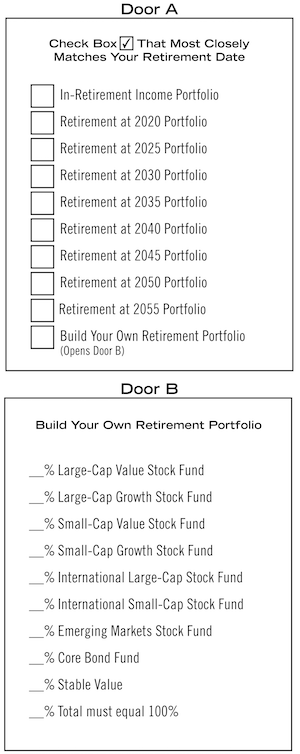

One way to accomplish this is to increase the visibility of the TDF options and to suppress the visibility of the single asset class funds. The TDFs are listed first in Door A, while Door B is activated only if a “self-build” option is selected (see examples).

Just as in the case of self-directed brokerage accounts (which have a very low uptake in most plans where they are offered), building one’s portfolio from single asset class funds ought to take some effort to implement. Regarding plan participants who really want to “roll their own,” we can assume they are savvy enough to find their way through the second door. Just as it is prudent to restrict access to self-directed brokerage accounts where participants can hurt themselves unless they are uniquely qualified, the same can be said regarding DC investors who (as the studies have shown) simply guess at their allocation, bereft of any analytical tools (e.g., Monte Carlo simulations, regression analysis, risk tolerance assessments, etc.).

Conclusion

Target-date funds will be the primary all-in-one asset allocation vehicle offered through DC plans for some years to come. The fact that most TDF investors are partial investors does not bode well for helping these DC investors achieve their optimal investment outcomes. The way forward is to implement choice architecture frameworks that better guide the average DC investor as they find their way through what is effectively a bunch of noise (multiple single asset class funds).

Providing the means for achieving a clearer understanding of TDFs will result in more professionally designed portfolios, which are tailored to what is arguably the most important risk factor in portfolio construction: one’s investment time horizon. And, as all plan advisors know, designing portfolios with as much clarity as possible helps to avoid unpleasant surprises in retirement.

Jerry Bramlett is the Managing Partner of Redstar Advisors and Managing Director of Sage Advisory Services. This column originally appeared in the Spring issue of NAPA Net the Magazine.