How do plan sponsors approach retaining retirees’ assets in the plan?

How do plan sponsors approach retaining retirees’ assets in the plan?

In any given month, retirement plan advisors and other industry professionals see more research than they can consume. When we encounter research-based articles that we don’t understand, or articles that tell a specific story, we normally spend more time on the ones that tell a specific story. Not that one fully understands everything we read or consume—but content that we do not comprehend, but that is generated by a credible and trusted source, gives us a reason to pause and reflect.

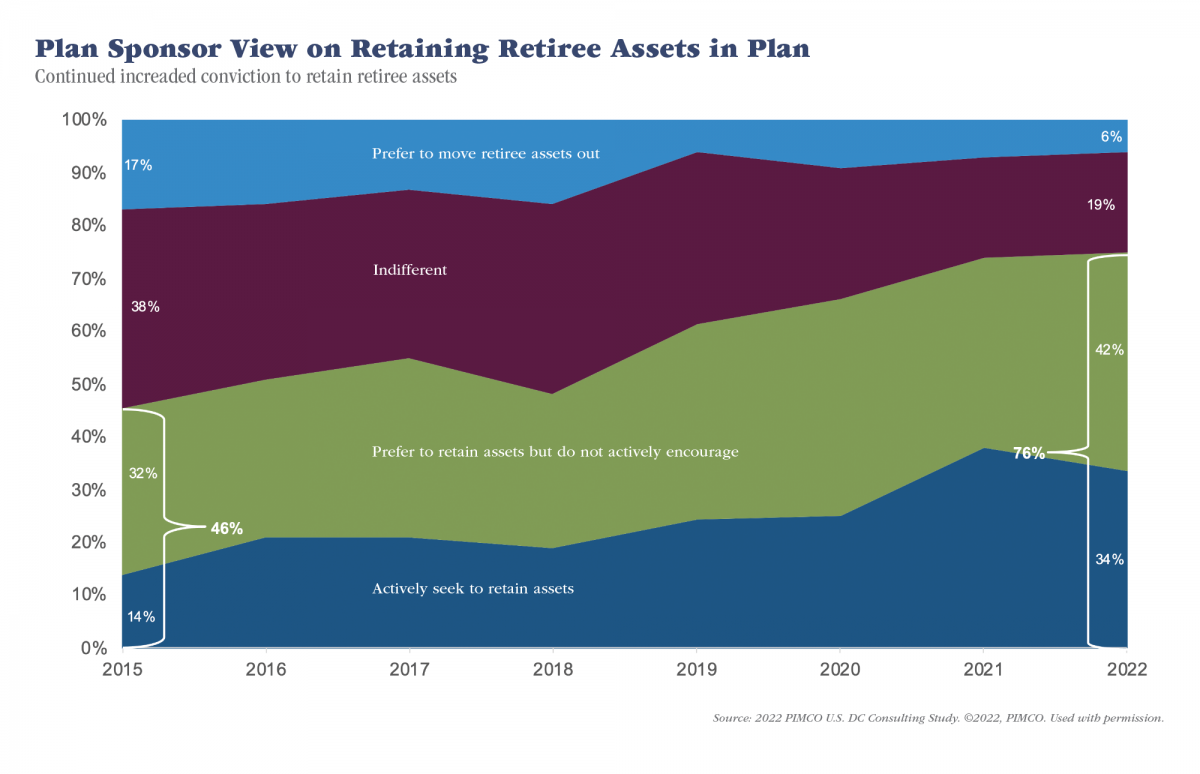

One such image, a graph titled “Plan Sponsor View on Retaining Retiree Assets” (see below) caught my attention recently, for several reasons. It tells a story that is counterintuitive to what I feel is logical and practical in today’s environment.

The “story” told in the image is the trend of some plan sponsors retaining more participant assets over the past six-plus years—both intentionally and passively—compared to other plan sponsors that prefer to move retiree assets out of the plan. If you take a moment to study the graph, you will likely find:

• a 65% reduction of plan sponsors seeking to move retirees out of the plan;

• a 50% reduction of plan sponsors who are indifferent; and

• a staggering increase among plan sponsors preferring to retain plan assets.

Why Retain Retirement Assets in the Plan?

First of all, there are many reasons to not retain participants’ assets following separation of service. Those reasons should always be considered before deciding to retain the plan assets of past plan participants. They include:

• Given the prevalence of ERISA litigation, with plan sponsors in plaintiffs’ crosshairs and retirement plan committee members who can be found personally liable for fiduciary breaches, what is the nexus for the trends represented in the graph?

• Accumulation of a retirement asset through prudent oversight of a 401(k) or 403(b) plan is a straight-forward objective. The goal is growth. Presumably, accumulation occurs at a rate commensurate with a participant’s comfort level with downside risk.

• When executed properly, decumulation of a retirement asset involves a complex set of options including—but not limited to—an understanding of securities, insurance, actuarial tables, tax law, risk tolerance, general health, and strong communication skills.

• Since many plan-driven insurance products purchased by the plan are based upon plan assets (i.e., fiduciary insurance, ERISA bonds, etc.) it might seem prudent to keep plan assets as low as possible. It seems also reasonable that a $15 million plan would carry lower premiums—and less overall fiduciary risk—than a $2 million plan.

Back to the “why.” There are just a handful of reasons for retaining past participant balances within a plan. They include:

• Since the plan sponsor has assisted all participants in amassing a solid retirement plan asset during their working years, it stands to reason that the plan sponsor may want to be a party to their journey through the retirement years. (At this point the company may have a paternalistic attitude towards each participant within the plan.)

• Observing a close relationship with retirees may be a motivating factor for existing employees, as both the employer and its retirees regard their relationship as extending well beyond the retirees’ working years.

• Fostering a lifelong relationship with former employees may be a stabilizing force in retaining the existing workforce.

• On average, fees may be less if the plan assets or plan participants are greater due to volume discounts.

Read more commentary from Steff Chalk here.

Misconceptions Around Misperceptions

• “My employer does not care about the fees in our plan.”

• “Fees in retirement plans are higher than I pay as an individual investor.”

• “Employer-sponsored plans have ‘extra’ or ‘hidden’ fees that negatively affect plan participants.”

Who would have thought there was so much to view and talk about in that one chart? I remain amazed by the overall trend to retain plan assets within a tax-qualified defined contribution plan.

Steff Chalk is the Executive Director of The Retirement Advisor University (TRAU), The Plan Sponsor University (TPSU) and 401kTV. This column first appeared in the Winter issue of NAPA Net the Magazine.